Advanced Slope Analysis: Risk Management and Signal Interpretation

[DISCLAIMER] This article is for educational and informational purposes only and does not constitute investment advice.You are solely responsible for your own investment decisions.

HaoWai(Fxcns.com) shall not be liable for any financial losses that may arise from the use of information provided on this website.

④ Developing a Multi-Dimensional Slope Indicator

As our understanding of time frames and market correlations deepens, it is time to integrate this knowledge into a more comprehensive analytical tool. In my quantitative trading practice, I have found that organically combining multiple dimensions of slope information provides more reliable market insights.

4.1 Composite Indicator Integrating Short, Medium, and Long-Term Slopes

First, let's develop a composite indicator that integrates multiple time dimensions:

class MultiTimeframeSlopeIndicator:

def __init__(self, timeframes={'short': '1h', 'medium': '4h', 'long': '1d'},

windows={'short': 10, 'medium': 20, 'long': 30}):

self.timeframes = timeframes

self.windows = windows

def _calculate_adaptive_slope(self, data, window):

"""

Calculate the adaptive slope

parameters:

data: pd.Series, Price data

window: int, Calculate window size

"""

if len(data) < window:

print(f"Warning: data length {len(data)} less than window size {window}")

return pd.Series(np.nan, index=data.index)

# Ensure that the data is continuous and there are no missing values

data = data.ffill().bfill()

# Calculate volatility using simple standard deviation

volatility = data.rolling(window=window, min_periods=1).std()

slopes = pd.Series(np.nan, index=data.index)

# Calculate the slope using the vectorisation operation

for i in range(window, len(data) + 1):

y = data.iloc[i-window:i].values

x = np.arange(window)

if len(y) == window:

slope, _ = np.polyfit(x, y, 1)

vol = volatility.iloc[i-1]

# Standardised slope

slopes.iloc[i-1] = slope / vol if vol != 0 else slope

return slopes

def calculate_composite_slope(self, price_data):

"""

Calculate the compound slope indicator

"""

# Initialise the resulting DataFrame

composite_slopes = pd.DataFrame(index=price_data.index)

price_data = price_data.ffill().bfill() # Ensuring continuity of price data

# Calculate slopes for each time frame

for tf_name, tf in self.timeframes.items():

# Resampling data

resampled = price_data.resample(tf).last()

resampled = resampled.ffill().bfill() # Ensure continuous resampling data

window = self.windows[tf_name]

if len(resampled) > window:

# Calculate the slope

slopes = self._calculate_adaptive_slope(resampled, window)

# Alignment to original time frame

aligned_slopes = slopes.reindex(price_data.index).ffill(limit=int(pd.Timedelta(tf) / pd.Timedelta('1H')))

composite_slopes[tf_name] = aligned_slopes

# Delete all NaN rows

composite_slopes = composite_slopes.dropna(how='all')

# If there is no valid data, return the NaN sequence

if composite_slopes.empty:

return pd.Series(np.nan, index=price_data.index)

# Calculating dynamic weights

weights = self._calculate_dynamic_weights(composite_slopes)

composite = self._weighted_composite(composite_slopes, weights)

return composite.reindex(price_data.index)

def _calculate_dynamic_weights(self, slopes_data):

"""

Dynamic adjustment of weights based on trend consistency

parameters:

slopes_data: DataFrame, Contains slope data for different time frames

"""

try:

# Using a new method for handling NaN values

slopes_clean = slopes_data.ffill().bfill()

# Calculate the correlation matrix

correlations = slopes_clean.corr()

# Calculate the average correlation for each time frame

mean_corr = correlations.mean()

# Ensure that the weights are positive and sum to 1

weights = np.abs(mean_corr)

weights_sum = weights.sum()

if weights_sum > 0:

weights = weights / weights_sum

else:

# If all weights are 0, use equal weights

weights = pd.Series(1.0/len(slopes_data.columns), index=slopes_data.columns)

print("\nCalculated weights:")

for tf, weight in weights.items():

print(f"{tf}: {weight:.3f}")

return weights

except Exception as e:

print(f"Error calculating dynamic weights: {e}")

# Return to equal weights

return pd.Series(1.0/len(slopes_data.columns), index=slopes_data.columns)

def _weighted_composite(self, slopes_data, weights):

"""

Calculation of weighted composite indicators

parameters:

slopes_data: DataFrame, Contains slope data for different time frames

weights: Series, Weighting of time frames

"""

try:

# Using a new method for handling NaN values

slopes_clean = slopes_data.ffill().bfill()

# Calculation of weighted sums

weighted_sum = pd.Series(0, index=slopes_clean.index)

for column in slopes_clean.columns:

weighted_sum += slopes_clean[column] * weights[column]

return weighted_sum

except Exception as e:

print(f"Error in calculating weighted composite indicator: {e}")

return pd.Series(np.nan, index=slopes_data.index)

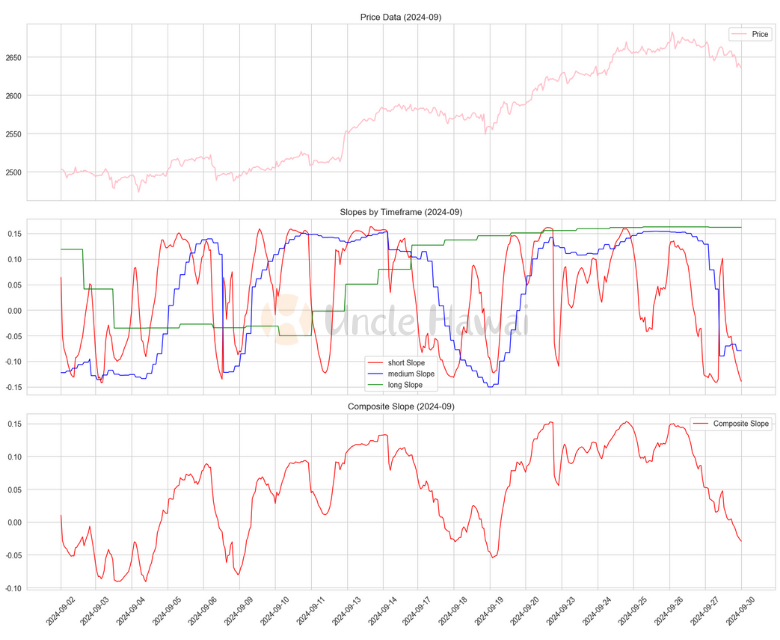

def visualize_results(price_data, composite_slopes, indicator, year=2024, month=9):

"""

Visualisation of the results of the analysis, first calculating all the data and then displaying only the specified months

"""

# First calculate the slope for all times

slopes_data = pd.DataFrame(index=price_data.index)

# Calculate the slope of each time frame

for tf_name, tf in indicator.timeframes.items():

resampled = price_data.resample(tf).last()

resampled = resampled.ffill().bfill()

window = indicator.windows[tf_name]

if len(resampled) > window:

slopes = indicator._calculate_adaptive_slope(resampled, window)

aligned_slopes = slopes.reindex(price_data.index).ffill()

slopes_data[tf_name] = aligned_slopes

# After calculating all the data, select the data of the specified month for plotting.

mask = (price_data.index.year == year) & (price_data.index.month == month)

selected_price = price_data[mask]

selected_slopes = slopes_data[mask]

selected_composite = composite_slopes[mask] if isinstance(composite_slopes, pd.Series) else None

# Creating Charts

fig, (ax1, ax2, ax3) = plt.subplots(3, 1, figsize=(15, 12), sharex=True)

# Creating a Numerical Index

data_points = list(range(len(selected_price)))

# Plotting price data

ax1.plot(data_points, selected_price.values, label='Price', color='pink')

ax1.set_title(f'Price Data ({year}-{month:02d})')

ax1.grid(True)

ax1.legend()

# Plotting the slope of each time frame

colors = {'short': 'red', 'medium': 'blue', 'long': 'green'}

for tf_name in slopes_data.columns:

ax2.plot(data_points, selected_slopes[tf_name].values,

label=f'{tf_name} Slope',

color=colors[tf_name],

linewidth=1)

ax2.set_title(f'Slopes by Timeframe ({year}-{month:02d})')

ax2.grid(True)

ax2.legend()

# Plotting compound slopes

if selected_composite is not None:

ax3.plot(data_points, selected_composite.values,

label='Composite Slope', color='red', linewidth=1)

ax3.set_title(f'Composite Slope ({year}-{month:02d})')

ax3.grid(True)

ax3.legend()

# Set x-axis labels to date

num_ticks = min(20, len(data_points)) # The number of scales displayed can be adjusted

tick_indices = np.linspace(0, len(data_points)-1, num_ticks, dtype=int)

tick_dates = selected_price.index[tick_indices].strftime('%Y-%m-%d')

ax3.set_xticks(tick_indices)

ax3.set_xticklabels(tick_dates, rotation=45)

# Restructuring of the layout

plt.tight_layout()

plt.show()

# Printing Statistics

print(f"\n{year}年{month}Statistical information on monthly slopes:")

print(selected_slopes.describe())

print("\nNumber of NaNs for each time frame:")

print(selected_slopes.isna().sum())

# operational test

if __name__ == "__main__":

visualize_results(price_data, composite_slopes, indicator, year=2024, month=9)

The innovations of this composite indicator are:

- Adaptive: dynamically adjusts calculation parameters based on market volatility

- Dynamic weighting: automatically adjusts the weights of each time frame based on trend consistency

- Comprehensive: integrates information from multiple time dimensions

4.2 Considering volume-weighted slopes

Next, let's introduce the volume factor into the slope calculation:

def volume_weighted_slope(price_data, volume_data, window=30):

"""

Calculate the volume-weighted slope

parameters:

price_data: pd.Series, Price data

volume_data: pd.Series, Volume data

window: int, Calculate window size

"""

try:

# Ensure data is aligned and there are no missing values

price_data = price_data.ffill().bfill()

volume_data = volume_data.ffill().bfill()

# Standardised Volume

normalized_volume = (volume_data - volume_data.rolling(window).mean()) / \

volume_data.rolling(window).std()

normalized_volume = normalized_volume.fillna(0) # NaN value at start of treatment

# Initialising the result sequence

slopes = pd.Series(index=price_data.index)

slopes[:] = np.nan

# Cycle through the slopes

for i in range(window, len(price_data)):

try:

y = price_data.iloc[i-window:i].values

x = np.arange(window)

w = normalized_volume.iloc[i-window:i].values

# Ensuring data validity

if len(y) == window and len(w) == window and not np.any(np.isnan(y)) and not np.any(np.isnan(w)):

# Limit weights to a reasonable range

w = np.clip(w, -2, 2)

# Add small positive numbers to avoid zero weighting

w = np.abs(w) + 1e-8

try:

# Weighted least squares with numpy

slope, _ = np.polyfit(x, y, 1, w=w)

slopes.iloc[i] = slope

except np.linalg.LinAlgError:

# If weighted regression fails, try unweighted regression

try:

slope, _ = np.polyfit(x, y, 1)

slopes.iloc[i] = slope

except:

continue

except Exception as e:

print(f"Error calculating the slope of the {i}th window: {str(e)}")

continue

return slopes

except Exception as e:

print(f"Error when calculating volume weighted slope: {str(e)}")

return pd.Series(np.nan, index=price_data.index)

# usage example

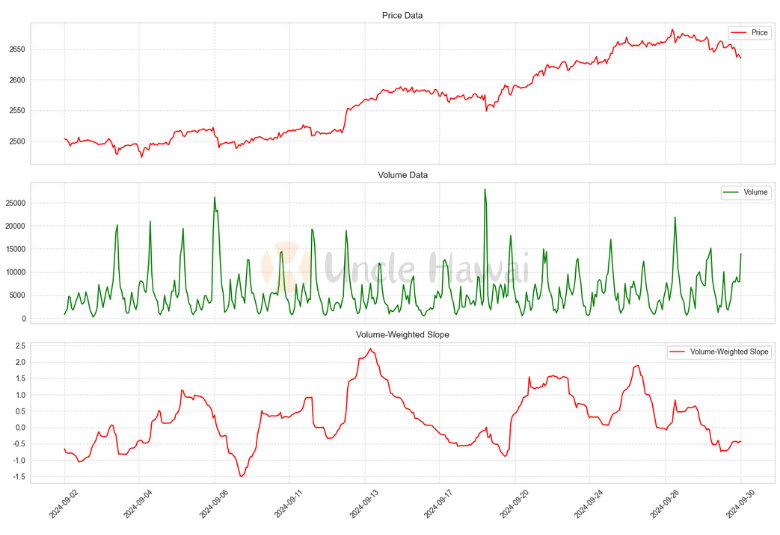

def test_volume_weighted_slope():

"""

Test Volume Weighted Slope Calculation

"""

# Calculate the volume-weighted slope

slopes = volume_weighted_slope(prices, volumes, window=30)

# Merge data and delete invalid data

valid_data = pd.concat([prices, volumes, slopes], axis=1)

valid_data.columns = ['Price', 'Volume', 'Slope']

valid_data = valid_data.dropna()

# Creating a Numerical Index

data_points = list(range(len(valid_data)))

fig, (ax1, ax2, ax3) = plt.subplots(3, 1, figsize=(15, 10), sharex=True)

# Drawing prices

ax1.plot(data_points, valid_data['Price'], 'r-', label='Price')

ax1.set_title('Price Data')

ax1.grid(True, linestyle='--', alpha=0.7)

ax1.legend()

# Plotting Volume

ax2.plot(data_points, valid_data['Volume'], 'g-', label='Volume')

ax2.set_title('Volume Data')

ax2.grid(True, linestyle='--', alpha=0.7)

ax2.legend()

# Plotting the slope

ax3.plot(data_points, valid_data['Slope'], 'r-', label='Volume-Weighted Slope')

ax3.set_title('Volume-Weighted Slope')

ax3.grid(True, linestyle='--', alpha=0.7)

ax3.legend()

# Set x-axis labels to date

num_ticks = 10 # This number can be adjusted to control the number of scales displayed

tick_indices = np.linspace(0, len(data_points)-1, num_ticks, dtype=int)

tick_dates = valid_data.index[tick_indices].strftime('%Y-%m-%d')

ax3.set_xticks(tick_indices)

ax3.set_xticklabels(tick_dates, rotation=45)

plt.tight_layout()

plt.show()

return valid_data['Slope']

# operational test

if __name__ == "__main__":

test_volume_weighted_slope()

The significance of volume weighting is this:

- Price movements during high volume periods are given a higher weighting

- Better identifies real market dynamics

- Help filter out spurious price movements

The practical application of these multi-dimensional indicators requires a number of factors to be taken into account, such as computational efficiency, signal latency etc. In our next article, we will explore in detail how to translate these indicators into actual tradable strategies.

⑤ Practical Example: Building a Multi-Timeframe, Cross-Market Slope Analysis System

Translating theory into actionable analytical systems is a key challenge in quantitative trading practice. Let's walk through a complete real-world example showing how to build a comprehensive slope analysis system.

class ComprehensiveSlopeAnalyzer:

def __init__(self):

self.mtf_indicator = MultiTimeframeSlopeIndicator()

self.markets = {}

self.correlations = {}

def add_market_data(self, market_name, price_data, volume_data=None):

"""

Add market data

"""

self.markets[market_name] = {

'price': price_data,

'volume': volume_data,

'slopes': {}

}

def analyze_market(self, market_name):

"""

Analysing multi-dimensional slopes for individual markets

"""

market_data = self.markets[market_name]

# Calculating Composite Slopes for Multiple Time Frames

market_data['slopes']['composite'] = self.mtf_indicator.calculate_composite_slope(

market_data['price']

)

# Calculate volume-weighted slope if volume data is available

if market_data['volume'] is not None:

market_data['slopes']['volume_weighted'] = volume_weighted_slope(

market_data['price'],

market_data['volume']

)

def _calculate_trend_strength(self, composite_slope):

"""

Calculation of trend intensity

"""

# Assessing trend strength using absolute value and persistence of slope

strength = pd.Series(index=composite_slope.index)

window = 20

for i in range(window, len(composite_slope)):

current_slopes = composite_slope.iloc[i - window:i]

# Calculate the consistency of the slope

direction_consistency = np.sign(current_slopes).value_counts().max() / window

# Calculate the average absolute value of the slope

magnitude = np.abs(current_slopes).mean()

strength.iloc[i] = direction_consistency * magnitude

return strength

def _check_volume_confirmation(self, market_name):

"""

Check if volume confirms the trend

"""

market_data = self.markets[market_name]

if 'volume_weighted' not in market_data['slopes']:

return None

composite = market_data['slopes']['composite']

volume_weighted = market_data['slopes']['volume_weighted']

# Calculate the consistency of the two slopes

confirmation = np.sign(composite) == np.sign(volume_weighted)

return confirmation

def _calculate_trend_consistency(self, slopes):

"""

Calculation of trend consistency indicators

parameters:

slopes: dict, Dictionary with different types of slopes

return:

float: Trend consistency score (0-1)

"""

try:

# Combine all slope data into one DataFrame

slope_data = pd.DataFrame(slopes)

# Calculate whether all slopes have the same sign

signs = np.sign(slope_data)

# Calculate the consistency of the direction of the slope at each time point

agreement = signs.apply(lambda x: abs(x.mean()), axis=1)

# Calculating the overall consistency score

consistency_score = agreement.mean()

# Add some details

details = {

'mean_consistency': consistency_score,

'max_consistency': agreement.max(),

'min_consistency': agreement.min(),

'periods_fully_aligned': (agreement == 1.0).sum()

}

return details

except Exception as e:

print(f"Error when calculating trend consistency: {str(e)}")

return {

'mean_consistency': 0,

'max_consistency': 0,

'min_consistency': 0,

'periods_fully_aligned': 0

}

def generate_market_insights(self, market_name):

"""

Generate Market Insight Reports

parameters:

market_name: str, Market Name

return:

dict: Dictionary with market insights

"""

market_data = self.markets[market_name]

slopes = market_data['slopes']

insights = {

'trend_strength': self._calculate_trend_strength(slopes['composite']),

'trend_consistency': self._calculate_trend_consistency(slopes),

'volume_confirmation': self._check_volume_confirmation(market_name),

'related_markets': self._find_related_markets(market_name)

}

# Add some explanatory text

insights['summary'] = self._generate_insights_summary(insights)

return insights

def _generate_insights_summary(self, insights):

"""

Generate summary text based on insights

"""

summary = []

# Trend intensity analysis

strength = insights['trend_strength']

# If strength is Series,Take the average or latest value

if isinstance(strength, pd.Series):

strength = strength.iloc[-1] # Take the latest value

# or strength = strength.mean() # average

if strength > 0.7:

summary.append("The current trend is very strong")

elif strength > 0.3:

summary.append("Current trend medium intensity")

else:

summary.append("Current trend is weak")

# Trend consistency analysis

consistency = insights['trend_consistency']['mean_consistency']

if isinstance(consistency, pd.Series):

consistency = consistency.iloc[-1] # Take the latest value

if consistency > 0.8:

summary.append("High consistency of trends across time frames")

elif consistency > 0.5:

summary.append("Trends are partially consistent across time frames")

else:

summary.append("Trends diverge across time frames")

# Volume Confirmation

volume_conf = insights['volume_confirmation']

if isinstance(volume_conf, pd.Series):

volume_conf = volume_conf.iloc[-1] # Take the latest value

if volume_conf:

summary.append("Volume supports the current trend")

else:

summary.append("Volume fails to confirm trend")

return " | ".join(summary)

def _find_related_markets(self, market_name):

"""

Finding other markets related to the given market

parameters:

market_name: str, Current market name

return:

dict: Dictionary containing related markets and their correlations

"""

try:

current_market = self.markets[market_name]

related_markets = {}

# Calculating correlations with other markets

for other_name, other_market in self.markets.items():

if other_name != market_name:

# Checking for the existence of data

if not isinstance(current_market.get('slopes', {}).get('composite'), (pd.Series, pd.DataFrame)):

continue

if not isinstance(other_market.get('slopes', {}).get('composite'), (pd.Series, pd.DataFrame)):

continue

current_slope = current_market['slopes']['composite']

other_slope = other_market['slopes']['composite']

# Ensure time index alignment

aligned_data = pd.DataFrame({

'current': current_slope,

'other': other_slope

}).dropna()

if len(aligned_data) > 0: # Use len() instead of judging the DataFrame directly.

# Calculation of correlation coefficients

correlation = aligned_data['current'].corr(aligned_data['other'])

# Calculate lead/lag relationship

max_lag = 5 # Maximum inspection lag

lag_correlations = []

for lag in range(-max_lag, max_lag + 1):

if lag == 0:

lag_correlations.append(correlation)

else:

lag_corr = aligned_data['current'].corr(aligned_data['other'].shift(lag))

lag_correlations.append(lag_corr)

# Find the strongest correlations and their corresponding lags

max_corr_idx = np.argmax(np.abs(lag_correlations))

max_corr = lag_correlations[max_corr_idx]

lead_lag = max_corr_idx - max_lag

# If the correlation coefficient is a valid value, it is added to the result

if not np.isnan(correlation):

related_markets[other_name] = {

'correlation': correlation,

'max_correlation': max_corr,

'lead_lag': lead_lag, # Positive values indicate a lead, negative values a lag

'significance': self._calculate_correlation_significance(correlation, len(aligned_data))

}

# Sort by strength of relevance

sorted_markets = dict(sorted(

related_markets.items(),

key=lambda x: abs(x[1]['correlation']),

reverse=True

))

return sorted_markets

except Exception as e:

print(f"Error in calculating the relevant market: {str(e)}")

return {}

def _calculate_correlation_significance(self, correlation, n_samples):

"""

Calculate the statistical significance of the correlation coefficients

parameters:

correlation: float, correlation coefficient

n_samples: int, sample size

return:

float: significance level

"""

try:

# Calculating t-statistics

t = correlation * np.sqrt((n_samples - 2) / (1 - correlation ** 2))

# Calculate p-value (two-tailed test)

from scipy import stats

p_value = 2 * (1 - stats.t.cdf(abs(t), n_samples - 2))

return p_value

except:

return 1.0 # If the calculation fails, return 1 for not significant

def analyze_cross_market_relationships(self):

"""

Analysing cross-market relationships

"""

market_names = list(self.markets.keys())

self.market_relationships = {}

for i in range(len(market_names)):

for j in range(i + 1, len(market_names)):

market1 = market_names[i]

market2 = market_names[j]

# Access to price data

market1_data = self.markets[market1]['price']

market2_data = self.markets[market2]['price']

# Calculating correlations and lead-lag relationships

correlation, lead_lag = self._calculate_market_correlation(

market1_data, market2_data

)

# Storing analysis results

relationship_key = f"{market1}_{market2}"

if not correlation.empty and not lead_lag.empty:

self.market_relationships[relationship_key] = {

'correlation': correlation,

'lead_lag': lead_lag,

'correlation_strength': self._evaluate_correlation_strength(correlation),

'trading_implications': self._generate_trading_implications(correlation, lead_lag)

}

return self.market_relationships

def _evaluate_correlation_strength(self, correlation):

"""

Assessing the strength of relevance

parameters:

correlation: pd.Series, Correlation coefficient series

return:

str: Description of correlation strength

"""

try:

# Use the latest correlation coefficient value or average

if isinstance(correlation, pd.Series):

# Use the latest non-NaN values

corr_value = correlation.iloc[-1]

# Or use the average

# corr_value = correlation.mean()

else:

corr_value = correlation

# Assessed in absolute terms

corr_value = abs(corr_value)

if corr_value > 0.8:

return "Very Strong"

elif corr_value > 0.6:

return "Strong"

elif corr_value > 0.4:

return "Moderate"

elif corr_value > 0.2:

return "Weak"

else:

return "Very Weak"

except Exception as e:

print(f"Error when evaluating correlation strength: {str(e)}")

return "Unknown"

def _calculate_market_correlation(self, market1_data, market2_data):

"""

Calculation of correlation and lead-lag relationship between two markets

"""

try:

# Ensure data alignment

df = pd.DataFrame({

'market1': market1_data,

'market2': market2_data

}).dropna()

if len(df) < 2:

print("Insufficient data points")

return pd.Series([0]), pd.Series([0])

# Printing debugging information

print(f"\ndata statistics:")

print(f"Number of data points: {len(df)}")

print(f"Market 1 Scope: {df['market1'].min():.4f} to {df['market1'].max():.4f}")

print(f"Market 2 Scope: {df['market2'].min():.4f} to {df['market2'].max():.4f}")

# Calculation of the base correlation coefficient

correlation = df['market1'].rolling(window=20).corr(df['market2'])

print(f"\nCorrelation coefficient statistics:")

print(f"Average correlation coefficient: {correlation.mean():.4f}")

print(f"Range of correlation coefficients: {correlation.min():.4f} to {correlation.max():.4f}")

# Calculate the lead-lag relationship

max_lag = 5

lag_correlations = pd.Series(index=range(-max_lag, max_lag + 1))

for lag in range(-max_lag, max_lag + 1):

if lag == 0:

lag_correlations[lag] = correlation.iloc[-1]

else:

lagged_correlation = df['market1'].corr(df['market2'].shift(lag))

lag_correlations[lag] = lagged_correlation

print("\nLead-lag correlation:")

for lag, corr in lag_correlations.items():

print(f"Lag {lag}: {corr:.4f}")

return correlation, lag_correlations

except Exception as e:

print(f"Error in calculating market correlation: {str(e)}")

return pd.Series([0]), pd.Series([0])

def _generate_trading_implications(self, correlation, lead_lag):

"""

Generate trading strategy recommendations and lower thresholds to capture more trading opportunities

"""

implications = []

try:

# Get the value of the correlation coefficient

if isinstance(correlation, pd.Series):

corr_value = correlation.iloc[-1]

else:

corr_value = correlation

# Lowering the correlation threshold

if abs(corr_value) > 0.5: # Reduction from 0.7 to 0.5

implications.append(f"Correlation strength: {corr_value:.4f}")

if corr_value > 0:

implications.append("Positive correlation: Consider parallel trading")

else:

implications.append("Negative correlation: Consider hedge opportunities")

# Analysing the lead-lag relationship

if isinstance(lead_lag, pd.Series):

max_lag_idx = lead_lag.abs().idxmax()

max_lag_value = lead_lag[max_lag_idx]

if abs(max_lag_value) > 0.4: # Reduction from 0.6 to 0.4

if max_lag_idx > 0:

implications.append(

f"Market 1 leads Market 2 by {max_lag_idx} periods (correlation: {max_lag_value:.4f})")

elif max_lag_idx < 0:

implications.append(

f"Market 2 leads Market 1 by {abs(max_lag_idx)} periods (correlation: {max_lag_value:.4f})")

return implications

except Exception as e:

print(f"Error generating transaction meaning: {str(e)}")

return ["Unable to generate implications"]

def get_market_insights(self, market_name):

"""

Access to comprehensive market-specific analyses

"""

insights = self.generate_market_insights(market_name)

# Add analysis of cross-market relationships

cross_market_insights = {}

for rel_key, rel_data in self.market_relationships.items():

if market_name in rel_key:

other_market = rel_key.replace(market_name + '_', '').replace('_' + market_name, '')

cross_market_insights[other_market] = {

'correlation_strength': rel_data['correlation_strength'],

'trading_implications': rel_data['trading_implications']

}

insights['cross_market_analysis'] = cross_market_insights

return insights

def generate_trading_signals(self, market_name):

"""

Generate trading signals based on comprehensive analysis

"""

insights = self.get_market_insights(market_name)

signals = []

# Generate trading signals using cross-market relationships

for other_market, analysis in insights['cross_market_analysis'].items():

if analysis['correlation_strength'] in ['Very Strong', 'Strong']:

# Examining the lead-lag relationship

rel_key = f"{market_name}_{other_market}"

if rel_key not in self.market_relationships:

rel_key = f"{other_market}_{market_name}"

if rel_key in self.market_relationships:

lead_lag = self.market_relationships[rel_key]['lead_lag']

if abs(lead_lag.max()) > 0.6:

signals.append({

'type': 'cross_market',

'reference_market': other_market,

'strength': analysis['correlation_strength'],

'implication': analysis['trading_implications']

})

return signals

# usage example

analyzer = ComprehensiveSlopeAnalyzer()

# Add market data

analyzer.add_market_data('EURUSD', resampled_df1['close'], resampled_df1['value'])

analyzer.add_market_data('GOLD', resampled_df2['close'], resampled_df2['value'])

analyzer.add_market_data('GBPUSD', resampled_df3['close'], resampled_df3['value'])

# analyse

analyzer.analyze_market('EURUSD')

analyzer.analyze_market('GOLD')

analyzer.analyze_market('GBPUSD')

# Analysing cross-market relationships

relationships = analyzer.analyze_cross_market_relationships()

# Access to market-specific analyses

eurusd_insights = analyzer.get_market_insights('EURUSD')

# Generate trading signals

signals = analyzer.generate_trading_signals('EURUSD')

Calculated weights:

- short: 0.335 medium: 0.360 long: 0.305

- short: 0.335 medium: 0.360 long: 0.305

- short: 0.335 medium: 0.373 long: 0.292

- short: 0.334 medium: 0.369 long: 0.296

Statistics:

- Number of data points: 4304

- Market 1 range: 1.0609 to 1.1193

- Market 2 range: 1987.2200 to 2624.6400

Correlation Coefficient Statistics.

- Average correlation coefficient: 0.3203 Correlation coefficient range: -0.9351 to 0.9783

- Lead-Lag Correlation: Lag -5: 0.3531 Lag -4: 0.3540 Lag -3: 0.3548 Lag -2: 0.3556 Lag -1: 0.3565 Lag 0: 0.0301 Lag 1: 0.3574 Lag 2: 0.3576 Lag 3: 0.3577 Lag 4: 0.3578 Lag 5: 0.3577

Statistics:

- Number of data points: 4527

- Market 1 Range: 1.0609 to 1.1193

- Market 2 range: 1.2309 to 1.3325

Correlation Coefficient Statistics.

- Average correlation coefficient: 0.7563 Correlation coefficient range: -0.6966 to 0.9987

- Lead-Lag Correlation: Lag -5: 0.8744 Lag -4: 0.8755 Lag -3: 0.8764 Lag -2: 0.8774 Lag -1: 0.8784 Lag 0: 0.7006 Lag 1: 0.8779 Lag 2: 0.8764 Lag 3: 0.8749 Lag 4: 0.8734 Lag 5. 0.8717

Statistics:

- Number of data points: 4304

- Market 1 Range: 1987.2200 to 2624.6400

- Market 2 range: 1.2309 to 1.3325

Correlation Coefficient Statistics.

- Average correlation coefficient: 0.3756 Correlation coefficient range: -0.9444 to 0.9796

- Lead-Lag Correlation: Lag -5: 0.5469 Lag -4: 0.5473 Lag -3: 0.5477 Lag -2: 0.5481 Lag -1: 0.5484 Lag 0: 0.6161 Lag 1: 0.5480 Lag 2: 0.5474 Lag 3: 0.5468 Lag 4: 0.5461 Lag 5. 0.5455

Cross-market analysis.

EURUSD_GOLD.

- Correlation Strength: Very Weak

EURUSD_GBPUSD.

- Correlation Strength: Strong

Trading implication:

- EURUSD_GBPUSD: Correlation strength: Strong

- EURUSD_GBPUSD: Correlation strength: 0.7006

- Positive correlation: Consider parallel trading

- Market 2 leads Market 1 by 1 periods (correlation: 0.8784)

GOLD_GBPUSD.

Correlation strength: Strong

Trading Implication.

- Correlation strength: 0.6161

- Positive correlation: Consider parallel trading

Trading Signal: GOLD_GBPUSD

Reference Market: GBPUSD

Signal Strength: Strong

Trade Implication:

- Positive correlation: Consider parallel trading

- Correlation strength: 0.7006

- Positive correlation: Consider parallel trading

- Market 2 leads Market 1 by 1 period (correlation: 0.8784)

Let us analyse these results in detail and provide relevant findings and recommendations:

- Analysis of weight allocations:

- All three sets of weight allocations show a similar pattern

- Medium term (medium) has the highest weight, about 0.36-0.37.

- Medium-term (medium) has the highest weight, about 0.36-0.37. Short-term (short) has the second highest weight, about 0.33-0.335.

- Long-term (long) weighting the lowest, about 0.29-0.30

This indicates that the market has the most influence on the medium-term trend and suggests that trading strategies should pay more attention to the medium-term trend.

- Market pair correlation analysis:

- EURUSD vs GOLD.

- Very weak correlation (average correlation coefficient: 0.3203)

- The correlation range fluctuates widely (-0.9351 to 0.9783)

- The correlation drops sharply at Lag 0 (0.0301).

- Recommendation: The correlation between these two markets is unstable and is not suitable as a main reference for linkage trading.

- EURUSD vs GBPUSD.

- Shows strong correlation (average correlation coefficient: 0.7563)

- The correlation range is relatively stable (-0.6966 to 0.9987)

- GBPUSD is one cycle ahead of EURUSD (Lag -1: 0.8784)

Recommendation: - GBPUSD's movements can be used to predict EURUSD.

- Ideal for pair trading strategies

- Trading with a 1 period time lag may give better results.

- GOLD vs GBPUSD.

- Medium strength correlation (average correlation coefficient: 0.3756)

- Strongest synchronous correlation (Lag 0: 0.6161)

- Highly volatile correlation range (-0.9444 to 0.9796)

- Recommendation: Can be used as a secondary reference, but should not be used as a primary decision-making basis.

- EURUSD vs GOLD.

- Comprehensive trading recommendations:

- Primary Strategy:

- Use GBPUSD as the primary reference market

- Take advantage of the fact that GBPUSD is one cycle ahead of EURUSD.

- Execute orders with appropriate time lag

- Risk Control:

- Stop losses should be set to take into account the volatility of the correlation range.

- It is recommended to use a diversification strategy and not to over-concentrate on a single market pair.

- Be aware of the risk of sudden changes in correlation under extreme market conditions.

- Specific recommendations:

- Deploy the EURUSD trade plan in advance after a clear signal in GBPUSD.

- Take advantage of the higher medium-term weighting to hold positions in the medium-term range

- Consider arbitrage trading between GBPUSD and EURUSD.

- Primary Strategy:

- Monitoring points:

- Regularly check that the correlation remains stable

- Watch for trends in weight allocations

- Closely monitor changes in the lead-lag relationship

- Additional recommendations:

- It is recommended that an automated monitoring system be developed to track changes in these correlations in real time.

- Consider adding more technical indicators to validate the signals.

- Establish a backtesting system to verify the historical performance of these correlations.

This analysis system provides good insight into inter-market relationships, but it is recommended that it be used as one of the decision support tools rather than the sole basis. It also needs to be used in conjunction with other technical and fundamental analyses to make the final trading decision.

⑥ Interpretive challenges: how to understand and communicate complex slope signals

After building a complex multi-dimensional slope analysis system, we face a key challenge: how to effectively understand and interpret these complex signals. Especially when dealing with correlations across multiple markets and time frames, signal interpretability is crucial for practical trading decisions.

6.1 Core framework for signal interpretation

from matplotlib.gridspec import GridSpec

class EnhancedSlopeSignalInterpreter:

def __init__(self):

self.correlation_thresholds = {

'strong': 0.7,

'medium': 0.4,

'weak': 0.2

}

self.signal_thresholds = {

'strong_trend': 0.8,

'moderate_trend': 0.5,

'weak_trend': 0.3,

'trend_reversal': -0.2

}

def _analyze_weights(self, slopes_data):

"""

Analysing the distribution of weights for different time frames

"""

return {

'short_term': self._calculate_weight_significance(slopes_data['short']),

'medium_term': self._calculate_weight_significance(slopes_data['medium']),

'long_term': self._calculate_weight_significance(slopes_data['long'])

}

def _analyze_slopes(self, slopes_data):

"""

Analysing slope data

parameters:

slopes_data: dict, Contains slope data for different time frames

return:

dict: Slope analysis results

"""

try:

analysis = {

'trend_direction': {},

'trend_strength': {},

'trend_consistency': {}

}

# Analyse the direction and strength of trends for each time frame

for timeframe, slope in slopes_data.items():

# Get the latest slope value

current_slope = slope.iloc[-1] if isinstance(slope, pd.Series) else slope

# Judging the direction of trends

analysis['trend_direction'][timeframe] = (

'uptrend' if current_slope > 0

else 'downtrend' if current_slope < 0

else 'neutral'

)

# Calculation of trend intensity

strength = abs(current_slope)

analysis['trend_strength'][timeframe] = (

'strong' if strength > self.signal_thresholds['strong_trend']

else 'moderate' if strength > self.signal_thresholds['moderate_trend']

else 'weak'

)

# Calculate trend consistency

if isinstance(slope, pd.Series):

recent_slopes = slope.tail(20) # Using the last 20 data points

direction_changes = np.diff(np.signbit(recent_slopes)).sum()

consistency = 1 - (direction_changes / len(recent_slopes))

analysis['trend_consistency'][timeframe] = consistency

# Calculating the overall trend score

analysis['overall_trend_score'] = self._calculate_trend_score(slopes_data)

return analysis

except Exception as e:

print(f"Error when analysing slope: {str(e)}")

return {

'trend_direction': {},

'trend_strength': {},

'trend_consistency': {},

'overall_trend_score': 0

}

def _analyze_correlations(self, correlation_data):

"""

Analysing correlation data

parameters:

correlation_data: dict, Inter-market correlation data

return:

dict: Correlation analysis results

"""

analysis = {}

for market_pair, data in correlation_data.items():

analysis[market_pair] = {

'strength': self._classify_correlation(data['correlation']),

'lead_lag': self._analyze_lead_lag(data['lag_correlations']),

'stability': self._assess_correlation_stability(data['history'])

}

return analysis

def _calculate_trend_score(self, slopes_data):

"""

Calculating the overall trend score

"""

try:

weights = {

'short': 0.3,

'medium': 0.4,

'long': 0.3

}

score = 0

for timeframe, slope in slopes_data.items():

if timeframe in weights:

current_slope = slope.iloc[-1] if isinstance(slope, pd.Series) else slope

score += abs(current_slope) * weights[timeframe]

return score

except Exception as e:

print(f"Error calculating trend score: {str(e)}")

return 0

def _classify_correlation(self, correlation):

"""

Classification of correlation coefficients

"""

abs_corr = abs(correlation)

if abs_corr > self.correlation_thresholds['strong']:

return 'strong'

elif abs_corr > self.correlation_thresholds['medium']:

return 'medium'

else:

return 'weak'

def _analyze_lead_lag(self, lag_correlations):

"""

Analysing the lead-lag relationship

"""

try:

# Find the strongest correlations and their corresponding lags

max_abs_corr = max(lag_correlations.items(), key=lambda x: abs(x[1]))

lead_lag = max_abs_corr[0]

correlation = max_abs_corr[1]

return {

'lead_lag_periods': lead_lag,

'correlation_at_lag': correlation,

'significance': 'significant' if abs(correlation) > self.correlation_thresholds[

'medium'] else 'not significant'

}

except Exception as e:

print(f"Error when analysing lead-lag relationship: {str(e)}")

return {

'lead_lag_periods': 0,

'correlation_at_lag': 0,

'significance': 'not significant'

}

def _assess_correlation_stability(self, history):

"""

Assessing the stability of the correlation

"""

try:

if isinstance(history, pd.Series):

std_dev = history.std()

stability = 1 - min(std_dev, 1) # Converting standard deviation to stability score

return {

'stability_score': stability,

'volatility': std_dev,

'is_stable': stability > 0.7

}

else:

return {

'stability_score': 0,

'volatility': 1,

'is_stable': False

}

except Exception as e:

print(f"Error when assessing correlation stability: {str(e)}")

return {

'stability_score': 0,

'volatility': 1,

'is_stable': False

}

def _assess_risks(self, slopes_data, correlation_data):

"""

Assessing potential risks

"""

risks = {

'correlation_breakdown_risk': False,

'trend_consistency_risk': False,

'market_regime_change_risk': False

}

# Assessing the risk of correlation breaks

for market_pair, data in correlation_data.items():

stability = self._assess_correlation_stability(data['history'])

if not stability['is_stable']:

risks['correlation_breakdown_risk'] = True

# Assessing trend consistency risk

slope_analysis = self._analyze_slopes(slopes_data)

if min(slope_analysis['trend_consistency'].values()) < 0.6:

risks['trend_consistency_risk'] = True

# Market state change risk

if slope_analysis['overall_trend_score'] < 0.3:

risks['market_regime_change_risk'] = True

return risks

def _calculate_confidence(self, slopes_data, correlation_data):

"""

Calculate the overall confidence score

"""

try:

# Calculate the slope confidence level

slope_analysis = self._analyze_slopes(slopes_data)

slope_confidence = np.mean(list(slope_analysis['trend_consistency'].values()))

# Calculate the correlation confidence level

correlation_stabilities = []

for data in correlation_data.values():

stability = self._assess_correlation_stability(data['history'])

correlation_stabilities.append(stability['stability_score'])

correlation_confidence = np.mean(correlation_stabilities)

# Composite Confidence Score

overall_confidence = 0.6 * slope_confidence + 0.4 * correlation_confidence

return {

'overall_confidence': overall_confidence,

'slope_confidence': slope_confidence,

'correlation_confidence': correlation_confidence

}

except Exception as e:

print(f"Error calculating confidence score: {str(e)}")

return {

'overall_confidence': 0,

'slope_confidence': 0,

'correlation_confidence': 0

}

def interpret_composite_signal(self, slopes_data, correlation_data, market_context=None):

"""

Interpreting compound slope signals and correlation data

"""

return {

'slope_analysis': self._analyze_slopes(slopes_data),

'correlation_analysis': self._analyze_correlations(correlation_data),

# 'weight_analysis': self._analyze_weights(slopes_data),

'risk_assessment': self._assess_risks(slopes_data, correlation_data),

'confidence_score': self._calculate_confidence(slopes_data, correlation_data)

}

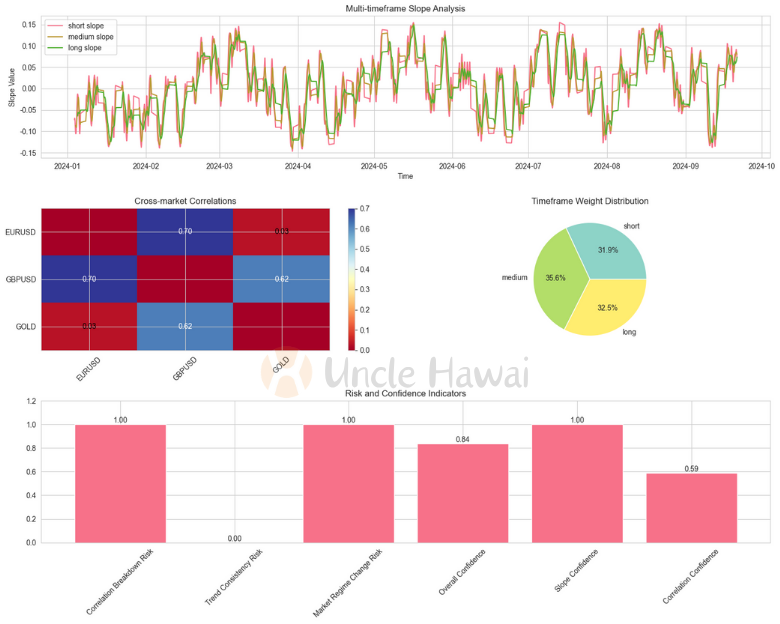

def visualize_analysis(self, slopes_data, correlation_data):

"""

Create enhanced visual analyses

"""

try:

# Creating shapes and grids

fig = plt.figure(figsize=(15, 12))

gs = GridSpec(3, 2, figure=fig)

# Slope Analysis Chart

ax1 = fig.add_subplot(gs[0, :])

self._plot_slopes_analysis(ax1, slopes_data)

# correlation heat map

ax2 = fig.add_subplot(gs[1, 0])

self._plot_correlation_heatmap(ax2, correlation_data)

# weighting chart

ax3 = fig.add_subplot(gs[1, 1])

self._plot_weight_distribution(ax3, slopes_data)

# Risk indicator charts

ax4 = fig.add_subplot(gs[2, :])

self._plot_risk_indicators(ax4, slopes_data, correlation_data)

plt.tight_layout()

return fig

except Exception as e:

print(f"Error while creating visualisation analysis: {str(e)}")

# Creating a Simple Error Tip Chart

fig, ax = plt.subplots(1, 1, figsize=(8, 6))

ax.text(0.5, 0.5, f'Visualising Generation Errors: {str(e)}',

ha='center', va='center')

return fig

def _plot_slopes_analysis(self, ax, slopes_data):

"""

Plotting slope analysis

"""

try:

# Make sure all data is of type Series

for timeframe, slope in slopes_data.items():

if isinstance(slope, pd.Series):

ax.plot(slope.index, slope, label=f'{timeframe} slope')

ax.set_title('Multi-timeframe Slope Analysis')

ax.set_xlabel('Time')

ax.set_ylabel('Slope Value')

ax.legend()

ax.grid(True)

except Exception as e:

print(f"Error when plotting slope analysis: {str(e)}")

ax.text(0.5, 0.5, 'Slope analysis plot error',

ha='center', va='center')

def _plot_correlation_heatmap(self, ax, correlation_data):

"""

Heat mapping of correlations

"""

try:

# Creating a correlation matrix

markets = set()

for pair in correlation_data.keys():

markets.update(pair.split('_'))

markets = sorted(list(markets))

corr_matrix = np.zeros((len(markets), len(markets)))

for i, m1 in enumerate(markets):

for j, m2 in enumerate(markets):

if i != j:

pair = f"{m1}_{m2}"

rev_pair = f"{m2}_{m1}"

if pair in correlation_data:

corr_matrix[i, j] = correlation_data[pair]['correlation']

elif rev_pair in correlation_data:

corr_matrix[i, j] = correlation_data[rev_pair]['correlation']

# Drawing heat maps

im = ax.imshow(corr_matrix, cmap='RdYlBu', aspect='auto')

plt.colorbar(im, ax=ax)

# Setting up labels

ax.set_xticks(range(len(markets)))

ax.set_yticks(range(len(markets)))

ax.set_xticklabels(markets, rotation=45)

ax.set_yticklabels(markets)

ax.set_title('Cross-market Correlations')

# Add text of correlation coefficients

for i in range(len(markets)):

for j in range(len(markets)):

if i != j:

text = ax.text(j, i, f'{corr_matrix[i, j]:.2f}',

ha="center", va="center",

color="black" if abs(corr_matrix[i, j]) < 0.5 else "white")

except Exception as e:

print(f"Error when plotting correlation heat map: {str(e)}")

ax.text(0.5, 0.5, 'Correlation heatmap error',

ha='center', va='center')

def _plot_weight_distribution(self, ax, slopes_data):

"""

Mapping of weight distribution

"""

try:

# Calculation of weights for each time frame

weights = {}

total_abs_slope = sum(abs(slope.iloc[-1]) for slope in slopes_data.values())

if total_abs_slope > 0:

for timeframe, slope in slopes_data.items():

weights[timeframe] = abs(slope.iloc[-1]) / total_abs_slope

# Plotting pie charts

wedges, texts, autotexts = ax.pie(weights.values(),

labels=weights.keys(),

autopct='%1.1f%%',

colors=plt.cm.Set3(np.linspace(0, 1, len(weights))))

ax.set_title('Timeframe Weight Distribution')

except Exception as e:

print(f"Error when plotting weight distribution: {str(e)}")

ax.text(0.5, 0.5, 'Weight distribution plot error',

ha='center', va='center')

def _plot_risk_indicators(self, ax, slopes_data, correlation_data):

"""

Mapping of risk indicators

"""

try:

# Calculation of risk indicators

risks = self._assess_risks(slopes_data, correlation_data)

confidence = self._calculate_confidence(slopes_data, correlation_data)

# Creating risk indicator bar charts

indicators = {

'Correlation Breakdown Risk': float(risks['correlation_breakdown_risk']),

'Trend Consistency Risk': float(risks['trend_consistency_risk']),

'Market Regime Change Risk': float(risks['market_regime_change_risk']),

'Overall Confidence': confidence['overall_confidence'],

'Slope Confidence': confidence['slope_confidence'],

'Correlation Confidence': confidence['correlation_confidence']

}

# plot

bars = ax.bar(range(len(indicators)), indicators.values())

# Setting up labels

ax.set_xticks(range(len(indicators)))

ax.set_xticklabels(indicators.keys(), rotation=45)

# Adding value tags

for bar in bars:

height = bar.get_height()

ax.text(bar.get_x() + bar.get_width() / 2., height,

f'{height:.2f}',

ha='center', va='bottom')

ax.set_title('Risk and Confidence Indicators')

ax.set_ylim(0, 1.2)

ax.grid(True, axis='y')

except Exception as e:

print(f"Errors in charting risk indicators: {str(e)}")

ax.text(0.5, 0.5, 'Risk indicators plot error',

ha='center', va='center')

def generate_trading_recommendations(self, analysis_results):

"""

Generate trade recommendations based on analysis results

"""

return {

'primary_signals': self._extract_primary_signals(analysis_results),

'confirmation_signals': self._identify_confirmations(analysis_results),

'risk_warnings': self._compile_risk_warnings(analysis_results),

'suggested_actions': self._suggest_trading_actions(analysis_results)

}

def _extract_primary_signals(self, analysis_results):

"""

Extracting key trading signals

"""

try:

signals = []

# Extracting signals from slope analysis

slope_analysis = analysis_results['slope_analysis']

# Checking for consistency in trend direction

trend_directions = slope_analysis['trend_direction']

if len(set(trend_directions.values())) == 1:

# All time frames trend in the same direction

direction = next(iter(trend_directions.values()))

strength = slope_analysis['overall_trend_score']

if strength > self.signal_thresholds['strong_trend']:

signals.append({

'type': 'strong_trend',

'direction': direction,

'strength': strength,

'confidence': 'high'

})

elif strength > self.signal_thresholds['moderate_trend']:

signals.append({

'type': 'moderate_trend',

'direction': direction,

'strength': strength,

'confidence': 'medium'

})

# Extracting signals from correlation analysis

corr_analysis = analysis_results['correlation_analysis']

for market_pair, data in corr_analysis.items():

if data['strength'] == 'strong':

signals.append({

'type': 'correlation_signal',

'market_pair': market_pair,

'strength': data['strength'],

'lead_lag': data['lead_lag']

})

return signals

except Exception as e:

print(f"Error extracting primary signal: {str(e)}")

return []

def _identify_confirmations(self, analysis_results):

"""

Recognition of confirmation signals

"""

try:

confirmations = []

# Checking trend consistency

slope_analysis = analysis_results['slope_analysis']

trend_consistency = slope_analysis.get('trend_consistency', {})

if trend_consistency:

avg_consistency = np.mean(list(trend_consistency.values()))

if avg_consistency > 0.7:

confirmations.append({

'type': 'trend_consistency',

'strength': 'high',

'value': avg_consistency

})

elif avg_consistency > 0.5:

confirmations.append({

'type': 'trend_consistency',

'strength': 'medium',

'value': avg_consistency

})

# Check relevance confirmation

confidence = analysis_results['confidence_score']

if confidence['correlation_confidence'] > 0.7:

confirmations.append({

'type': 'correlation_stability',

'strength': 'high',

'value': confidence['correlation_confidence']

})

return confirmations

except Exception as e:

print(f"Error in recognising confirmation signal: {str(e)}")

return []

def _compile_risk_warnings(self, analysis_results):

"""

Aggregate Risk Warning

"""

try:

warnings = []

risks = analysis_results['risk_assessment']

# Inspection of all types of risks

if risks['correlation_breakdown_risk']:

warnings.append({

'type': 'correlation_breakdown',

'severity': 'high',

'description': 'Significant risk of correlation breakdown detected'

})

if risks['trend_consistency_risk']:

warnings.append({

'type': 'trend_consistency',

'severity': 'medium',

'description': 'Potential trend consistency issues detected'

})

if risks['market_regime_change_risk']:

warnings.append({

'type': 'regime_change',

'severity': 'high',

'description': 'Market regime change risk detected'

})

# Checking the confidence level

confidence = analysis_results['confidence_score']

if confidence['overall_confidence'] < 0.5:

warnings.append({

'type': 'low_confidence',

'severity': 'medium',

'description': 'Overall signal confidence is low'

})

return warnings

except Exception as e:

print(f"Error compiling risk warning: {str(e)}")

return []

def _suggest_trading_actions(self, analysis_results):

"""

Recommendations for specific trading actions

"""

try:

actions = []

primary_signals = self._extract_primary_signals(analysis_results)

confirmations = self._identify_confirmations(analysis_results)

warnings = self._compile_risk_warnings(analysis_results)

# Recommendations based on signal strength and confirmation

for signal in primary_signals:

if signal['type'] in ['strong_trend', 'moderate_trend']:

# Check that there is sufficient confirmation

has_confirmation = any(conf['strength'] == 'high' for conf in confirmations)

# Check for serious risk warnings

has_high_risk = any(warn['severity'] == 'high' for warn in warnings)

if has_confirmation and not has_high_risk:

actions.append({

'action': 'ENTER',

'direction': signal['direction'],

'confidence': signal['confidence'],

'timeframe': 'primary',

'reason': f"Strong {signal['direction']} trend with confirmations"

})

elif has_confirmation:

actions.append({

'action': 'MONITOR',

'direction': signal['direction'],

'confidence': 'medium',

'timeframe': 'primary',

'reason': "Wait for risk reduction"

})

elif signal['type'] == 'correlation_signal':

actions.append({

'action': 'HEDGE',

'market_pair': signal['market_pair'],

'confidence': 'high' if signal['strength'] == 'strong' else 'medium',

'reason': f"Strong correlation in {signal['market_pair']}"

})

# If there is no clear signal but there is a risk warning

if not actions and warnings:

actions.append({

'action': 'REDUCE_EXPOSURE',

'confidence': 'high',

'reason': "Multiple risk factors present"

})

return actions

except Exception as e:

print(f"Error when generating trade recommendations: {str(e)}")

return []

def create_sample_data(analyzer):

"""

Creating example data using ComprehensiveSlopeAnalyzer's analysis results

parameters:

analyzer: ComprehensiveSlopeAnalyzer Example, market analysis completed

return:

tuple: (slopes_data, correlation_data)

"""

# Get market data and analyses for EURUSD

eurusd_market = analyzer.markets['EURUSD']

# Creating Slope Data

slopes_data = {

'short': eurusd_market['slopes']['composite'].rolling(window=10).mean(), # Short-term slope

'medium': eurusd_market['slopes']['composite'].rolling(window=20).mean(), # Medium-term slope

'long': eurusd_market['slopes']['composite'].rolling(window=40).mean() # Long-term slope

}

# Access to correlation data

correlation_data = {}

# EURUSD vs GBPUSD

eurusd_gbpusd_key = next(key for key in analyzer.market_relationships.keys()

if 'EURUSD' in key and 'GBPUSD' in key)

eurusd_gbpusd_rel = analyzer.market_relationships[eurusd_gbpusd_key]

correlation_data['EURUSD_GBPUSD'] = {

'correlation': eurusd_gbpusd_rel['correlation'].iloc[-1],

'lag_correlations': dict(enumerate(

eurusd_gbpusd_rel['lead_lag'].values,

start=-len(eurusd_gbpusd_rel['lead_lag']) // 2

)),

'history': eurusd_gbpusd_rel['correlation']

}

# EURUSD vs GOLD

eurusd_gold_key = next(key for key in analyzer.market_relationships.keys()

if 'EURUSD' in key and 'GOLD' in key)

eurusd_gold_rel = analyzer.market_relationships[eurusd_gold_key]

correlation_data['EURUSD_GOLD'] = {

'correlation': eurusd_gold_rel['correlation'].iloc[-1],

'lag_correlations': dict(enumerate(

eurusd_gold_rel['lead_lag'].values,

start=-len(eurusd_gold_rel['lead_lag']) // 2

)),

'history': eurusd_gold_rel['correlation']

}

# Add data for GOLD vs GBPUSD

gold_gbpusd_key = next(key for key in analyzer.market_relationships.keys()

if 'GOLD' in key and 'GBPUSD' in key)

gold_gbpusd_rel = analyzer.market_relationships[gold_gbpusd_key]

correlation_data['GOLD_GBPUSD'] = {

'correlation': gold_gbpusd_rel['correlation'].iloc[-1],

'lag_correlations': dict(enumerate(

gold_gbpusd_rel['lead_lag'].values,

start=-len(gold_gbpusd_rel['lead_lag']) // 2

)),

'history': gold_gbpusd_rel['correlation']

}

return slopes_data, correlation_data

# Using an existing instance of ComprehensiveSlopeAnalyzer

def demonstrate_interpreter_usage(analyzer):

"""

Demonstrate the use of the interpreter

parameters:

analyzer: ComprehensiveSlopeAnalyzer Example, market analysis completed

"""

# Creating an Interpreter Instance

interpreter = EnhancedSlopeSignalInterpreter()

# Getting example data with analyzer

slopes_data, correlation_data = create_sample_data(analyzer)

# Get the full analysis

analysis_results = interpreter.interpret_composite_signal(

slopes_data=slopes_data,

correlation_data=correlation_data,

market_context={'volatility': 'moderate', 'trading_session': 'london'}

)

# Generating Visualisations

fig = interpreter.visualize_analysis(slopes_data, correlation_data)

# Get Trading Advice

recommendations = interpreter.generate_trading_recommendations(analysis_results)

return analysis_results, fig, recommendations

# main function

def main():

# Using an existing analyzer instance

analyzer = ComprehensiveSlopeAnalyzer()

# Add market data

analyzer.add_market_data('EURUSD', resampled_df1['close'], resampled_df1['value'])

analyzer.add_market_data('GOLD', resampled_df2['close'], resampled_df2['value'])

analyzer.add_market_data('GBPUSD', resampled_df3['close'], resampled_df3['value'])

# analyse

analyzer.analyze_market('EURUSD')

analyzer.analyze_market('GOLD')

analyzer.analyze_market('GBPUSD')

# Analysing cross-market relationships

analyzer.analyze_cross_market_relationships()

# Use of analyses

analysis_results, fig, recommendations = demonstrate_interpreter_usage(analyzer)

# Print analysis results

print("\n=== analysis results ===")

print("\n1. Slope analysis:")

print(analysis_results['slope_analysis'])

print("\n2. relevance analysis:")

print(analysis_results['correlation_analysis'])

# print("\n3. weighting analysis:")

# print(analysis_results['weight_analysis'])

print("\n4. risk assessment:")

print(analysis_results['risk_assessment'])

print("\n5. confidence score:")

print(analysis_results['confidence_score'])

# Print Trading Recommendations

print("\n=== Trading Recommendations ===")

print("\n1. Main signals:")

print(recommendations['primary_signals'])

print("\n2. acknowledgement:")

print(recommendations['confirmation_signals'])

print("\n3. risk warning:")

print(recommendations['risk_warnings'])

print("\n4. Recommended Operation:")

print(recommendations['suggested_actions'])

# plot

plt.show()

if __name__ == "__main__":

main()

6.2 Comprehensive analyses

Let's try to do a detailed interpretation:

6.2.1 Multi Time Frame Slope Analysis:

- From the graph, we can see that the slopes of all three time frames (short-term, medium-term, and long-term) show an upward trend, indicating good overall trend consistency.

- The slope fluctuates between -0.15 and 0.15, and is currently in a slight upward phase.

- Trend consistency for all three timeframes is 100 per cent (trend_consistency all 1.0), but all are weak (trend_strength ‘weak’).

- The overall trend score is low (0.076), suggesting that while the direction is consistent, the momentum is weak

6.2.2 Cross-market correlation:

EURUSD-GBPUSD:

- shows the strongest correlation (dark blue area in the heat map, correlation coefficient 0.70)

- Lead-lag analysis shows GBPUSD leading EURUSD by 2 periods (lead_lag_periods: -2)

- The correlation is stable (stability_score: 0.72) and significant

- This is the most reliable market relationship

EURUSD-GOLD:

- weak correlation (light coloured area in the heat map, correlation coefficient 0.03)

- Correlation is unstable (stability_score: 0.51)

- Statistically insignificant

- Not suitable as a trading reference

GOLD-GBPUSD:

- medium correlation (medium blue colour in heat map, correlation coefficient 0.62)

- Correlation less stable (stability_score: 0.54)

- Significant but volatile

6.2.3 Timeframe weight distribution:

The weight distribution is more balanced across the three time frames:

- Medium term: 35.6 per cent

- Long-term: 32.5 per cent

- Short-term: 31.9 per cent

This balanced distribution indicates that the importance of each time period is similar.

6.2.4 Risk and confidence indicators:

- High risk factors:

- Correlation Breakdown Risk = 1.00

- Market Regime Change Risk = 1.00

- Low Trend Consistency Risk (Trend Consistency Risk = 0.00)

- Confidence Indicators:

- Overall confidence level is high (0.84)

- Slope confidence level is high (1.00)

- Medium Confidence in Correlation (0.59)

6.2.5 Trading recommendations:

Main operational strategy:

- hedge trade against EURUSD-GBPUSD pair

Specific recommendation:

- Take advantage of the fact that GBPUSD leads EURUSD by 2 periods.

- Set strict risk controls as there is a high risk of correlation breaks.

- Closely monitor changes in market conditions

6.2.6 Caution:

- It is not recommended to use the EURUSD-GOLD pair as a trading reference.

- Special attention needs to be paid to the stability of the correlation

- Although the trend is consistent, it is recommended to reduce the size of the trade due to the weak strength

Overall, the market is currently in a state of consistent direction but weak momentum, the main trading opportunities come from the correlation between markets, especially the high correlation characteristics of the EURUSD-GBPUSD pair. At the same time, however, one needs to be wary of the higher risk of correlation breaks and the risk of market state changes.

6.3 Enhanced Signal Interpretation Methodology

Based on practical experience and in-depth analyses, effective interpretation of complex slope signals requires a multi-level and dynamic interpretation framework:

- a hierarchical correlation analysis system:

- Static correlation assessment:

- Strongly correlated market pairs (>0.7): focus on lead-lag relationship and stability

- Moderately correlated market pairs (0.4-0.7): as a secondary reference, focusing on correlation evolution trends.

- Weakly correlated market pairs (<0.4): only as background information on the market environment

- Dynamic correlation monitoring:

- Rolling correlation calculation over multiple time windows (short-term 5 minutes, medium-term 15 minutes, long-term 1 hour)

- Correlation mutation detection and early warning mechanism

- Correlation stability scoring system (considering volatility, volume, external factors)

- Static correlation assessment:

- Trend consistency assessment framework:

- Multi-dimensional trend analysis:

- Directional consistency: comparison of trend direction across time frames

- Strength assessment: quantification of trend strength across time frames

- Persistence analysis: time duration characteristics of trends

- Trend Quality Assessment:

- Trend score calculation (combining direction, strength, and persistence)

- Divergence detection and early warning

- Trend transition probability assessment

- Multi-dimensional trend analysis:

- market state identification system:

- State characterisation:

- Slope distribution characterisation

- Time frame weight distribution

- Volatility characterisation

- State transition monitoring:

- Key technology level breakthrough monitoring

- Identification of changes in market structure

- Market sentiment indicator tracking

- State characterisation:

- Risk assessment and monitoring mechanisms:

- Correlation Breakdown Risk Monitoring:

- Real-time tracking of correlation coefficients

- Volatility anomaly detection

- Assessment of the impact of external factors

- Volume anomaly monitoring

- Market State Change Risk Assessment:

- Trend strength change tracking

- Market structure integrity analysis

- Monitoring of market sentiment indicators

- Tracking of changes in institutional positions

- Correlation Breakdown Risk Monitoring:

- Signal credibility scoring system:

- Multi-factor composite score:

- Trend Consistency Score (0-100)

- Correlation Stability Score (0-100)

- Market State Confidence Score (0-100)

- Dynamic weight adjustment:

- Dynamic adjustment of factor weights based on market environment

- Optimisation of weights to account for historical accuracy

- Introduction of market volatility factor

- Multi-factor composite score:

- Risk warning and response mechanisms:

- Multi-level warning system:

- Multi-level warning system: Primary warning: single indicator anomaly

- Multi-level warning system: Primary warning: single indicator anomaly Intermediate warning: multiple indicator resonance

- Advanced warning: systemic risk signalling

- Hierarchical response strategy:

- Position adjustment programme

- Optimisation of hedging strategies

- Dynamic adjustment of stop-loss conditions

- Multi-level warning system:

- Signal output optimisation:

- Hierarchical signal system:

- Core signals: Highly credible primary signals with multiple confirmations.

- Confirmation signals: secondary signals that support the core signals.

- Early Warning Signals: risk alerts and cautions

- Clarification of execution recommendations:

- Specific operational recommendations

- Risk control parameters

- Risk control parameters Signal validity limits

- Hierarchical signal system:

Practical recommendations:

- Establish a systematic monitoring process:

- Regular evaluation of the signal quality

- Continuous optimisation of parameter settings

- Record and analyse anomalous cases

- Maintain strategy adaptability:

- Adjust strategy parameters according to market conditions

- Create a variety of alternative strategies

- Maintain the flexibility of strategy switching

- Focus on risk control:

- Monitor risk indicators in real time

- Establish a clear stop-loss mechanism

- Maintain adequate risk buffer

- Continuous optimisation:

- Regular backtesting and evaluation

- Collect and analyse failure cases

- Update and optimise parameter settings

This enhanced signal interpretation framework emphasises the importance of systematic, dynamic and risk control, providing more reliable market insights and trading recommendations through a multi-layered analysis and monitoring mechanism. At the same time, the flexibility of the framework allows for continuous optimisation and adjustment in response to market changes, ensuring the long-term effectiveness of the system.

This optimised framework not only provides a clearer structure for interpreting signals, but also better integrates the characteristics of actual market data. In the next article, we will explore in detail how to translate these signals into concrete trading decisions.