全方位斜率(下):掌握跨时间跨市场的趋势洞察

[免责声明] 本文仅供教育和信息目的,不构成投资建议。您需对自身的投资决策承担全部责任。

浩外(Fxcns.com)对因使用本网站提供的信息而可能造成的任何财务损失概不负责。

④ 开发多维度斜率指标

随着我们对时间框架和市场关联性的理解加深,是时候将这些知识整合成一个更全面的分析工具了。在量化交易实践中,我发现将多个维度的斜率信息有机结合,能够提供更可靠的市场洞察。

4.1 综合短期、中期和长期斜率的复合指标

首先,让我们开发一个整合多个时间维度的复合指标:

class MultiTimeframeSlopeIndicator:

def __init__(self, timeframes={'short': '1h', 'medium': '4h', 'long': '1d'},

windows={'short': 10, 'medium': 20, 'long': 30}):

self.timeframes = timeframes

self.windows = windows

def _calculate_adaptive_slope(self, data, window):

"""

计算自适应斜率

参数:

data: pd.Series, 价格数据

window: int, 计算窗口大小

"""

if len(data) < window:

print(f"警告: 数据长度 {len(data)} 小于窗口大小 {window}")

return pd.Series(np.nan, index=data.index)

# 确保数据是连续的,没有缺失值

data = data.ffill().bfill()

# 计算波动率,使用简单标准差

volatility = data.rolling(window=window, min_periods=1).std()

slopes = pd.Series(np.nan, index=data.index)

# 使用向量化操作计算斜率

for i in range(window, len(data) + 1):

y = data.iloc[i-window:i].values

x = np.arange(window)

if len(y) == window:

slope, _ = np.polyfit(x, y, 1)

vol = volatility.iloc[i-1]

# 标准化斜率

slopes.iloc[i-1] = slope / vol if vol != 0 else slope

return slopes

def calculate_composite_slope(self, price_data):

"""

计算复合斜率指标

"""

# 初始化结果DataFrame

composite_slopes = pd.DataFrame(index=price_data.index)

price_data = price_data.ffill().bfill() # 确保价格数据连续

# 为每个时间框架计算斜率

for tf_name, tf in self.timeframes.items():

# 重采样数据

resampled = price_data.resample(tf).last()

resampled = resampled.ffill().bfill() # 确保重采样数据连续

window = self.windows[tf_name]

if len(resampled) > window:

# 计算斜率

slopes = self._calculate_adaptive_slope(resampled, window)

# 对齐到原始时间框架

aligned_slopes = slopes.reindex(price_data.index).ffill(limit=int(pd.Timedelta(tf) / pd.Timedelta('1H')))

composite_slopes[tf_name] = aligned_slopes

# 删除全部为NaN的行

composite_slopes = composite_slopes.dropna(how='all')

# 如果没有有效数据,返回NaN序列

if composite_slopes.empty:

return pd.Series(np.nan, index=price_data.index)

# 计算动态权重

weights = self._calculate_dynamic_weights(composite_slopes)

composite = self._weighted_composite(composite_slopes, weights)

return composite.reindex(price_data.index)

def _calculate_dynamic_weights(self, slopes_data):

"""

基于趋势一致性动态调整权重

参数:

slopes_data: DataFrame, 包含不同时间框架的斜率数据

"""

try:

# 使用新的方法处理NaN值

slopes_clean = slopes_data.ffill().bfill()

# 计算相关性矩阵

correlations = slopes_clean.corr()

# 计算每个时间框架的平均相关性

mean_corr = correlations.mean()

# 确保权重为正且和为1

weights = np.abs(mean_corr)

weights_sum = weights.sum()

if weights_sum > 0:

weights = weights / weights_sum

else:

# 如果所有权重都是0,使用均等权重

weights = pd.Series(1.0/len(slopes_data.columns), index=slopes_data.columns)

print("\n计算的权重:")

for tf, weight in weights.items():

print(f"{tf}: {weight:.3f}")

return weights

except Exception as e:

print(f"计算动态权重时出错: {e}")

# 返回均等权重

return pd.Series(1.0/len(slopes_data.columns), index=slopes_data.columns)

def _weighted_composite(self, slopes_data, weights):

"""

计算加权综合指标

参数:

slopes_data: DataFrame, 包含不同时间框架的斜率数据

weights: Series, 各时间框架的权重

"""

try:

# 使用新的方法处理NaN值

slopes_clean = slopes_data.ffill().bfill()

# 计算加权和

weighted_sum = pd.Series(0, index=slopes_clean.index)

for column in slopes_clean.columns:

weighted_sum += slopes_clean[column] * weights[column]

return weighted_sum

except Exception as e:

print(f"计算加权综合指标时出错: {e}")

return pd.Series(np.nan, index=slopes_data.index)

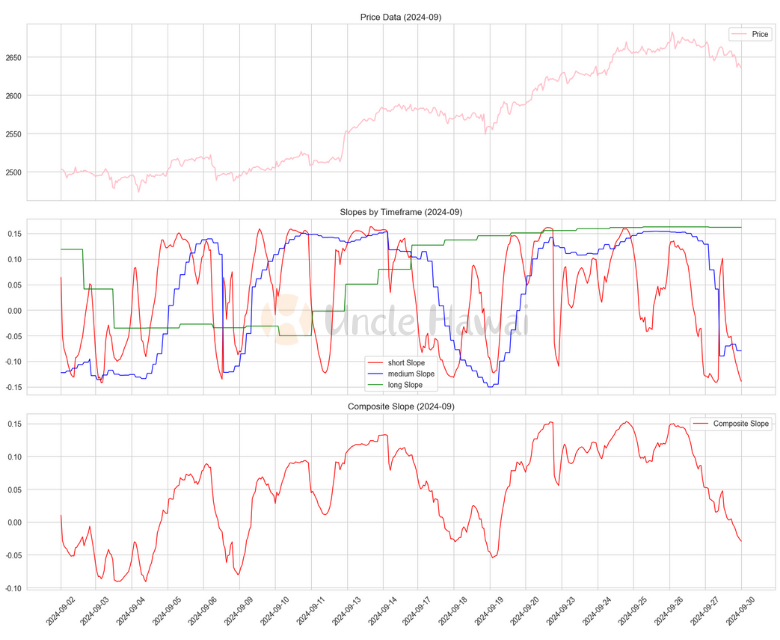

def visualize_results(price_data, composite_slopes, indicator, year=2024, month=9):

"""

可视化分析结果,先计算所有数据,然后只显示指定月份

"""

# 先计算所有时间的斜率

slopes_data = pd.DataFrame(index=price_data.index)

# 计算各时间框架的斜率

for tf_name, tf in indicator.timeframes.items():

resampled = price_data.resample(tf).last()

resampled = resampled.ffill().bfill()

window = indicator.windows[tf_name]

if len(resampled) > window:

slopes = indicator._calculate_adaptive_slope(resampled, window)

aligned_slopes = slopes.reindex(price_data.index).ffill()

slopes_data[tf_name] = aligned_slopes

# 在计算完所有数据后,选择指定月份的数据进行绘图

mask = (price_data.index.year == year) & (price_data.index.month == month)

selected_price = price_data[mask]

selected_slopes = slopes_data[mask]

selected_composite = composite_slopes[mask] if isinstance(composite_slopes, pd.Series) else None

# 创建图表

fig, (ax1, ax2, ax3) = plt.subplots(3, 1, figsize=(15, 12), sharex=True)

# 创建数字索引

data_points = list(range(len(selected_price)))

# 绘制价格数据

ax1.plot(data_points, selected_price.values, label='Price', color='pink')

ax1.set_title(f'Price Data ({year}-{month:02d})')

ax1.grid(True)

ax1.legend()

# 绘制各时间框架的斜率

colors = {'short': 'red', 'medium': 'blue', 'long': 'green'}

for tf_name in slopes_data.columns:

ax2.plot(data_points, selected_slopes[tf_name].values,

label=f'{tf_name} Slope',

color=colors[tf_name],

linewidth=1)

ax2.set_title(f'Slopes by Timeframe ({year}-{month:02d})')

ax2.grid(True)

ax2.legend()

# 绘制复合斜率

if selected_composite is not None:

ax3.plot(data_points, selected_composite.values,

label='Composite Slope', color='red', linewidth=1)

ax3.set_title(f'Composite Slope ({year}-{month:02d})')

ax3.grid(True)

ax3.legend()

# 设置x轴标签为日期

num_ticks = min(20, len(data_points)) # 可以调整显示的刻度数量

tick_indices = np.linspace(0, len(data_points)-1, num_ticks, dtype=int)

tick_dates = selected_price.index[tick_indices].strftime('%Y-%m-%d')

ax3.set_xticks(tick_indices)

ax3.set_xticklabels(tick_dates, rotation=45)

# 调整布局

plt.tight_layout()

plt.show()

# 打印统计信息

print(f"\n{year}年{month}月斜率统计信息:")

print(selected_slopes.describe())

print("\n各时间框架的NaN数量:")

print(selected_slopes.isna().sum())

# 运行测试

if __name__ == "__main__":

visualize_results(price_data, composite_slopes, indicator, year=2024, month=9)

这个复合指标的创新之处在于:

- 自适应性:根据市场波动性动态调整计算参数

- 动态权重:基于趋势一致性自动调整各时间框架的权重

- 综合性:整合了多个时间维度的信息

4.2 考虑成交量的加权斜率

接下来,让我们在斜率计算中引入成交量因素:

def volume_weighted_slope(price_data, volume_data, window=30):

"""

计算成交量加权斜率

参数:

price_data: pd.Series, 价格数据

volume_data: pd.Series, 成交量数据

window: int, 计算窗口大小

"""

try:

# 确保数据对齐且没有缺失值

price_data = price_data.ffill().bfill()

volume_data = volume_data.ffill().bfill()

# 标准化成交量

normalized_volume = (volume_data - volume_data.rolling(window).mean()) / \

volume_data.rolling(window).std()

normalized_volume = normalized_volume.fillna(0) # 处理开始的NaN值

# 初始化结果序列

slopes = pd.Series(index=price_data.index)

slopes[:] = np.nan

# 循环计算斜率

for i in range(window, len(price_data)):

try:

y = price_data.iloc[i-window:i].values

x = np.arange(window)

w = normalized_volume.iloc[i-window:i].values

# 确保数据有效

if len(y) == window and len(w) == window and not np.any(np.isnan(y)) and not np.any(np.isnan(w)):

# 将权重限制在合理范围内

w = np.clip(w, -2, 2)

# 添加小的正数以避免零权重

w = np.abs(w) + 1e-8

try:

# 使用numpy的加权最小二乘

slope, _ = np.polyfit(x, y, 1, w=w)

slopes.iloc[i] = slope

except np.linalg.LinAlgError:

# 如果加权回归失败,尝试不加权的回归

try:

slope, _ = np.polyfit(x, y, 1)

slopes.iloc[i] = slope

except:

continue

except Exception as e:

print(f"计算第 {i} 个窗口的斜率时出错: {str(e)}")

continue

return slopes

except Exception as e:

print(f"计算成交量加权斜率时出错: {str(e)}")

return pd.Series(np.nan, index=price_data.index)

# 使用示例

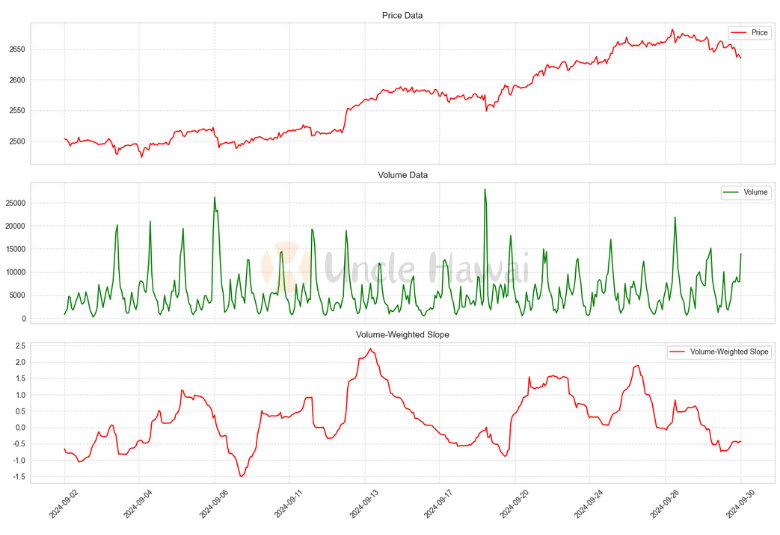

def test_volume_weighted_slope():

"""

测试成交量加权斜率计算

"""

# 计算成交量加权斜率

slopes = volume_weighted_slope(prices, volumes, window=30)

# 合并数据并删除无效数据

valid_data = pd.concat([prices, volumes, slopes], axis=1)

valid_data.columns = ['Price', 'Volume', 'Slope']

valid_data = valid_data.dropna()

# 创建数字索引

data_points = list(range(len(valid_data)))

fig, (ax1, ax2, ax3) = plt.subplots(3, 1, figsize=(15, 10), sharex=True)

# 绘制价格

ax1.plot(data_points, valid_data['Price'], 'r-', label='Price')

ax1.set_title('Price Data')

ax1.grid(True, linestyle='--', alpha=0.7)

ax1.legend()

# 绘制成交量

ax2.plot(data_points, valid_data['Volume'], 'g-', label='Volume')

ax2.set_title('Volume Data')

ax2.grid(True, linestyle='--', alpha=0.7)

ax2.legend()

# 绘制斜率

ax3.plot(data_points, valid_data['Slope'], 'r-', label='Volume-Weighted Slope')

ax3.set_title('Volume-Weighted Slope')

ax3.grid(True, linestyle='--', alpha=0.7)

ax3.legend()

# 设置x轴标签为日期

num_ticks = 10 # 可以调整这个数字来控制显示的刻度数量

tick_indices = np.linspace(0, len(data_points)-1, num_ticks, dtype=int)

tick_dates = valid_data.index[tick_indices].strftime('%Y-%m-%d')

ax3.set_xticks(tick_indices)

ax3.set_xticklabels(tick_dates, rotation=45)

plt.tight_layout()

plt.show()

return valid_data['Slope']

# 运行测试

if __name__ == "__main__":

test_volume_weighted_slope()

成交量加权的意义在于:

- 高成交量时段的价格变动获得更高权重

- 能够更好地识别真实的市场动力

- 帮助过滤虚假的价格波动

这些多维度指标的实际应用需要考虑很多因素,比如计算效率、信号延迟等。在我们的下一篇文章中,我们将详细探讨如何将这些指标转化为实际可交易的策略。

⑤ 实战示例:构建多时间框架、跨市场的斜率分析系统

在量化交易实践中,将理论转化为可操作的分析系统是一个关键挑战。让我们通过一个完整的实战案例,展示如何构建一个综合的斜率分析系统。

class ComprehensiveSlopeAnalyzer:

def __init__(self):

self.mtf_indicator = MultiTimeframeSlopeIndicator()

self.markets = {}

self.correlations = {}

def add_market_data(self, market_name, price_data, volume_data=None):

"""

添加市场数据

"""

self.markets[market_name] = {

'price': price_data,

'volume': volume_data,

'slopes': {}

}

def analyze_market(self, market_name):

"""

分析单个市场的多维度斜率

"""

market_data = self.markets[market_name]

# 计算多时间框架复合斜率

market_data['slopes']['composite'] = self.mtf_indicator.calculate_composite_slope(

market_data['price']

)

# 如果有成交量数据,计算成交量加权斜率

if market_data['volume'] is not None:

market_data['slopes']['volume_weighted'] = volume_weighted_slope(

market_data['price'],

market_data['volume']

)

def _calculate_trend_strength(self, composite_slope):

"""

计算趋势强度

"""

# 使用斜率的绝对值和持续性评估趋势强度

strength = pd.Series(index=composite_slope.index)

window = 20

for i in range(window, len(composite_slope)):

current_slopes = composite_slope.iloc[i - window:i]

# 计算斜率的一致性

direction_consistency = np.sign(current_slopes).value_counts().max() / window

# 计算斜率的平均绝对值

magnitude = np.abs(current_slopes).mean()

strength.iloc[i] = direction_consistency * magnitude

return strength

def _check_volume_confirmation(self, market_name):

"""

检查成交量是否确认趋势

"""

market_data = self.markets[market_name]

if 'volume_weighted' not in market_data['slopes']:

return None

composite = market_data['slopes']['composite']

volume_weighted = market_data['slopes']['volume_weighted']

# 计算两种斜率的一致性

confirmation = np.sign(composite) == np.sign(volume_weighted)

return confirmation

def _calculate_trend_consistency(self, slopes):

"""

计算趋势的一致性指标

参数:

slopes: dict, 包含不同类型斜率的字典

返回:

float: 趋势一致性得分 (0-1)

"""

try:

# 将所有斜率数据合并到一个DataFrame中

slope_data = pd.DataFrame(slopes)

# 计算所有斜率的符号是否一致

signs = np.sign(slope_data)

# 计算每个时间点上斜率方向的一致性

agreement = signs.apply(lambda x: abs(x.mean()), axis=1)

# 计算整体一致性得分

consistency_score = agreement.mean()

# 添加一些详细信息

details = {

'mean_consistency': consistency_score,

'max_consistency': agreement.max(),

'min_consistency': agreement.min(),

'periods_fully_aligned': (agreement == 1.0).sum()

}

return details

except Exception as e:

print(f"计算趋势一致性时出错: {str(e)}")

return {

'mean_consistency': 0,

'max_consistency': 0,

'min_consistency': 0,

'periods_fully_aligned': 0

}

def generate_market_insights(self, market_name):

"""

生成市场洞察报告

参数:

market_name: str, 市场名称

返回:

dict: 包含市场洞察的字典

"""

market_data = self.markets[market_name]

slopes = market_data['slopes']

insights = {

'trend_strength': self._calculate_trend_strength(slopes['composite']),

'trend_consistency': self._calculate_trend_consistency(slopes),

'volume_confirmation': self._check_volume_confirmation(market_name),

'related_markets': self._find_related_markets(market_name)

}

# 添加一些解释性文字

insights['summary'] = self._generate_insights_summary(insights)

return insights

def _generate_insights_summary(self, insights):

"""

根据洞察生成摘要文字

"""

summary = []

# 趋势强度分析

strength = insights['trend_strength']

# 如果strength是Series,取其平均值或最新值

if isinstance(strength, pd.Series):

strength = strength.iloc[-1] # 取最新值

# 或者 strength = strength.mean() # 取平均值

if strength > 0.7:

summary.append("当前趋势非常强劲")

elif strength > 0.3:

summary.append("当前趋势中等强度")

else:

summary.append("当前趋势较弱")

# 趋势一致性分析

consistency = insights['trend_consistency']['mean_consistency']

if isinstance(consistency, pd.Series):

consistency = consistency.iloc[-1] # 取最新值

if consistency > 0.8:

summary.append("不同时间框架的趋势高度一致")

elif consistency > 0.5:

summary.append("不同时间框架的趋势部分一致")

else:

summary.append("不同时间框架的趋势存在分歧")

# 成交量确认

volume_conf = insights['volume_confirmation']

if isinstance(volume_conf, pd.Series):

volume_conf = volume_conf.iloc[-1] # 取最新值

if volume_conf:

summary.append("成交量支持当前趋势")

else:

summary.append("成交量未能确认趋势")

return " | ".join(summary)

def _find_related_markets(self, market_name):

"""

寻找与给定市场相关的其他市场

参数:

market_name: str, 当前市场名称

返回:

dict: 包含相关市场及其相关性的字典

"""

try:

current_market = self.markets[market_name]

related_markets = {}

# 计算与其他市场的相关性

for other_name, other_market in self.markets.items():

if other_name != market_name:

# 检查数据是否存在

if not isinstance(current_market.get('slopes', {}).get('composite'), (pd.Series, pd.DataFrame)):

continue

if not isinstance(other_market.get('slopes', {}).get('composite'), (pd.Series, pd.DataFrame)):

continue

current_slope = current_market['slopes']['composite']

other_slope = other_market['slopes']['composite']

# 确保时间索引对齐

aligned_data = pd.DataFrame({

'current': current_slope,

'other': other_slope

}).dropna()

if len(aligned_data) > 0: # 使用 len() 而不是直接判断 DataFrame

# 计算相关系数

correlation = aligned_data['current'].corr(aligned_data['other'])

# 计算领先/滞后关系

max_lag = 5 # 最大检查的滞后期数

lag_correlations = []

for lag in range(-max_lag, max_lag + 1):

if lag == 0:

lag_correlations.append(correlation)

else:

lag_corr = aligned_data['current'].corr(aligned_data['other'].shift(lag))

lag_correlations.append(lag_corr)

# 找出最强的相关性及其对应的滞后期

max_corr_idx = np.argmax(np.abs(lag_correlations))

max_corr = lag_correlations[max_corr_idx]

lead_lag = max_corr_idx - max_lag

# 如果相关系数是有效的数值,则添加到结果中

if not np.isnan(correlation):

related_markets[other_name] = {

'correlation': correlation,

'max_correlation': max_corr,

'lead_lag': lead_lag, # 正值表示领先,负值表示滞后

'significance': self._calculate_correlation_significance(correlation, len(aligned_data))

}

# 按相关性强度排序

sorted_markets = dict(sorted(

related_markets.items(),

key=lambda x: abs(x[1]['correlation']),

reverse=True

))

return sorted_markets

except Exception as e:

print(f"计算相关市场时出错: {str(e)}")

return {}

def _calculate_correlation_significance(self, correlation, n_samples):

"""

计算相关系数的统计显著性

参数:

correlation: float, 相关系数

n_samples: int, 样本数量

返回:

float: 显著性水平

"""

try:

# 计算t统计量

t = correlation * np.sqrt((n_samples - 2) / (1 - correlation ** 2))

# 计算p值(双尾检验)

from scipy import stats

p_value = 2 * (1 - stats.t.cdf(abs(t), n_samples - 2))

return p_value

except:

return 1.0 # 如果计算失败,返回1表示不显著

def analyze_cross_market_relationships(self):

"""

分析跨市场关系

"""

market_names = list(self.markets.keys())

self.market_relationships = {}

for i in range(len(market_names)):

for j in range(i + 1, len(market_names)):

market1 = market_names[i]

market2 = market_names[j]

# 获取价格数据

market1_data = self.markets[market1]['price']

market2_data = self.markets[market2]['price']

# 计算相关性和领先-滞后关系

correlation, lead_lag = self._calculate_market_correlation(

market1_data, market2_data

)

# 存储分析结果

relationship_key = f"{market1}_{market2}"

if not correlation.empty and not lead_lag.empty:

self.market_relationships[relationship_key] = {

'correlation': correlation,

'lead_lag': lead_lag,

'correlation_strength': self._evaluate_correlation_strength(correlation),

'trading_implications': self._generate_trading_implications(correlation, lead_lag)

}

return self.market_relationships

def _evaluate_correlation_strength(self, correlation):

"""

评估相关性强度

参数:

correlation: pd.Series, 相关系数序列

返回:

str: 相关性强度的描述

"""

try:

# 使用最新的相关系数值或平均值

if isinstance(correlation, pd.Series):

# 使用最新的非NaN值

corr_value = correlation.iloc[-1]

# 或者使用平均值

# corr_value = correlation.mean()

else:

corr_value = correlation

# 取绝对值进行评估

corr_value = abs(corr_value)

if corr_value > 0.8:

return "Very Strong"

elif corr_value > 0.6:

return "Strong"

elif corr_value > 0.4:

return "Moderate"

elif corr_value > 0.2:

return "Weak"

else:

return "Very Weak"

except Exception as e:

print(f"评估相关性强度时出错: {str(e)}")

return "Unknown"

def _calculate_market_correlation(self, market1_data, market2_data):

"""

计算两个市场之间的相关性和领先-滞后关系

"""

try:

# 确保数据对齐

df = pd.DataFrame({

'market1': market1_data,

'market2': market2_data

}).dropna()

if len(df) < 2:

print("数据点不足")

return pd.Series([0]), pd.Series([0])

# 打印调试信息

print(f"\n数据统计:")

print(f"数据点数量: {len(df)}")

print(f"市场1范围: {df['market1'].min():.4f} to {df['market1'].max():.4f}")

print(f"市场2范围: {df['market2'].min():.4f} to {df['market2'].max():.4f}")

# 计算基础相关系数

correlation = df['market1'].rolling(window=20).corr(df['market2'])

print(f"\n相关系数统计:")

print(f"平均相关系数: {correlation.mean():.4f}")

print(f"相关系数范围: {correlation.min():.4f} to {correlation.max():.4f}")

# 计算领先-滞后关系

max_lag = 5

lag_correlations = pd.Series(index=range(-max_lag, max_lag + 1))

for lag in range(-max_lag, max_lag + 1):

if lag == 0:

lag_correlations[lag] = correlation.iloc[-1]

else:

lagged_correlation = df['market1'].corr(df['market2'].shift(lag))

lag_correlations[lag] = lagged_correlation

print("\n领先-滞后相关性:")

for lag, corr in lag_correlations.items():

print(f"Lag {lag}: {corr:.4f}")

return correlation, lag_correlations

except Exception as e:

print(f"计算市场相关性时出错: {str(e)}")

return pd.Series([0]), pd.Series([0])

def _generate_trading_implications(self, correlation, lead_lag):

"""

生成交易策略建议,降低阈值以捕捉更多的交易机会

"""

implications = []

try:

# 获取相关系数的值

if isinstance(correlation, pd.Series):

corr_value = correlation.iloc[-1]

else:

corr_value = correlation

# 降低相关性阈值

if abs(corr_value) > 0.5: # 从0.7降低到0.5

implications.append(f"Correlation strength: {corr_value:.4f}")

if corr_value > 0:

implications.append("Positive correlation: Consider parallel trading")

else:

implications.append("Negative correlation: Consider hedge opportunities")

# 分析领先-滞后关系

if isinstance(lead_lag, pd.Series):

max_lag_idx = lead_lag.abs().idxmax()

max_lag_value = lead_lag[max_lag_idx]

if abs(max_lag_value) > 0.4: # 从0.6降低到0.4

if max_lag_idx > 0:

implications.append(

f"Market 1 leads Market 2 by {max_lag_idx} periods (correlation: {max_lag_value:.4f})")

elif max_lag_idx < 0:

implications.append(

f"Market 2 leads Market 1 by {abs(max_lag_idx)} periods (correlation: {max_lag_value:.4f})")

return implications

except Exception as e:

print(f"生成交易含义时出错: {str(e)}")

return ["Unable to generate implications"]

def get_market_insights(self, market_name):

"""

获取特定市场的综合分析结果

"""

insights = self.generate_market_insights(market_name)

# 添加跨市场关系的分析

cross_market_insights = {}

for rel_key, rel_data in self.market_relationships.items():

if market_name in rel_key:

other_market = rel_key.replace(market_name + '_', '').replace('_' + market_name, '')

cross_market_insights[other_market] = {

'correlation_strength': rel_data['correlation_strength'],

'trading_implications': rel_data['trading_implications']

}

insights['cross_market_analysis'] = cross_market_insights

return insights

def generate_trading_signals(self, market_name):

"""

基于综合分析生成交易信号

"""

insights = self.get_market_insights(market_name)

signals = []

# 使用跨市场关系生成交易信号

for other_market, analysis in insights['cross_market_analysis'].items():

if analysis['correlation_strength'] in ['Very Strong', 'Strong']:

# 检查领先-滞后关系

rel_key = f"{market_name}_{other_market}"

if rel_key not in self.market_relationships:

rel_key = f"{other_market}_{market_name}"

if rel_key in self.market_relationships:

lead_lag = self.market_relationships[rel_key]['lead_lag']

if abs(lead_lag.max()) > 0.6:

signals.append({

'type': 'cross_market',

'reference_market': other_market,

'strength': analysis['correlation_strength'],

'implication': analysis['trading_implications']

})

return signals

# 使用示例

analyzer = ComprehensiveSlopeAnalyzer()

# 添加市场数据

analyzer.add_market_data('EURUSD', resampled_df1['close'], resampled_df1['value'])

analyzer.add_market_data('GOLD', resampled_df2['close'], resampled_df2['value'])

analyzer.add_market_data('GBPUSD', resampled_df3['close'], resampled_df3['value'])

# 进行分析

analyzer.analyze_market('EURUSD')

analyzer.analyze_market('GOLD')

analyzer.analyze_market('GBPUSD')

# 分析跨市场关系

relationships = analyzer.analyze_cross_market_relationships()

# 获取特定市场的分析结果

eurusd_insights = analyzer.get_market_insights('EURUSD')

# 生成交易信号

signals = analyzer.generate_trading_signals('EURUSD')

计算的权重:

- short: 0.335 medium: 0.360 long: 0.305

- short: 0.335 medium: 0.373 long: 0.292

- short: 0.334 medium: 0.369 long: 0.296

EURUSD_GOLD:

数据统计:

- 数据点数量: 4304

- 市场1范围: 1.0609 to 1.1193

- 市场2范围: 1987.2200 to 2624.6400

相关系数统计:

- 平均相关系数: 0.3203 相关系数范围: -0.9351 to 0.9783

- 领先-滞后相关性:Lag -5: 0.3531 Lag -4: 0.3540 Lag -3: 0.3548 Lag -2: 0.3556 Lag -1: 0.3565 Lag 0: 0.0301 Lag 1: 0.3574 Lag 2: 0.3576 Lag 3: 0.3577 Lag 4: 0.3578 Lag 5: 0.3577

EURUSD_GBPUSD:

数据统计:

- 数据点数量: 4527

- 市场1范围: 1.0609 to 1.1193

- 市场2范围: 1.2309 to 1.3325

相关系数统计:

- 平均相关系数: 0.7563 相关系数范围: -0.6966 to 0.9987

- 领先-滞后相关性: Lag -5: 0.8744 Lag -4: 0.8755 Lag -3: 0.8764 Lag -2: 0.8774 Lag -1: 0.8784 Lag 0: 0.7006 Lag 1: 0.8779 Lag 2: 0.8764 Lag 3: 0.8749 Lag 4: 0.8734 Lag 5: 0.8717

数据统计: 数据点数量: 4304

- 市场1范围: 1987.2200 to 2624.6400

- 市场2范围: 1.2309 to 1.3325

相关系数统计:

- 平均相关系数: 0.3756 相关系数范围: -0.9444 to 0.9796

- 领先-滞后相关性: Lag -5: 0.5469 Lag -4: 0.5473 Lag -3: 0.5477 Lag -2: 0.5481 Lag -1: 0.5484 Lag 0: 0.6161 Lag 1: 0.5480 Lag 2: 0.5474 Lag 3: 0.5468 Lag 4: 0.5461 Lag 5: 0.5455

跨市场关系分析:

EURUSD_GOLD:

- 相关性强度: Very Weak

EURUSD_GBPUSD:

- 相关性强度: Strong

- 交易含义:

- Correlation strength: 0.7006

- Positive correlation: Consider parallel trading

- Market 2 leads Market 1 by 1 periods (correlation: 0.8784)

GOLD_GBPUSD:

- 相关性强度: Strong

- 交易含义:

- Correlation strength: 0.6161

- Positive correlation: Consider parallel trading

- 交易信号:

- 参考市场: GBPUSD

- 信号强度: Strong

- 交易含义:

- Correlation strength: 0.7006

- Positive correlation: Consider parallel trading

- Market 2 leads Market 1 by 1 periods (correlation: 0.8784)

让我们详细分析这些结果并提供相关发现与建议:

- 权重分配分析:

- 三组权重分配都显示出相似的模式

- 中期(medium)权重最高,约0.36-0.37

- 短期(short)次之,约0.33-0.335

- 长期(long)权重最低,约0.29-0.30

这表明市场在中期趋势上的影响力最大,建议交易策略应该更多地关注中期走势。

- 市场对相关性分析:

- EURUSD vs GOLD:

- 相关性很弱(平均相关系数:0.3203)

- 相关范围波动很大(-0.9351 到 0.9783)

- Lag 0时相关性急剧下降(0.0301)

建议:这两个市场之间的相关性不稳定,不适合作为联动交易的主要参考。

- EURUSD vs GBPUSD:

- 显示出强相关性(平均相关系数:0.7563)

- 相关范围相对稳定(-0.6966 到 0.9987)

- GBPUSD领先EURUSD一个周期(Lag -1: 0.8784)

建议: - 可以利用GBPUSD的走势来预测EURUSD

- 适合进行配对交易策略

- 设置1个周期的时间差进行交易可能获得更好的效果

- GOLD vs GBPUSD:

- 中等强度相关性(平均相关系数:0.3756)

- 同步相关性最强(Lag 0: 0.6161)

- 相关范围波动较大(-0.9444 到 0.9796)

建议:可以作为辅助参考,但不应作为主要决策依据。

- EURUSD vs GOLD:

- 综合交易建议:

- 主要策略:

- 将GBPUSD作为主要参考市场

- 利用GBPUSD领先EURUSD一个周期的特性进行交易

- 设置适当的时间差执行订单

- 风险控制:

- 设置止损时需考虑相关性范围的波动

- 建议使用分散投资策略,不要过度集中在单一市场对

- 在极端市场条件下需警惕相关性突变风险

- 具体操作建议:

- 在GBPUSD出现明确信号后,可提前部署EURUSD的交易计划

- 利用中期权重较高的特点,将持仓时间定在中期范围内

- 可以考虑在GBPUSD和EURUSD之间进行套利交易

- 主要策略:

- 监控要点:

- 定期检查相关性是否保持稳定

- 关注权重分配的变化趋势

- 密切监控领先-滞后关系的变化

- 补充建议:

- 建议开发自动化监控系统,实时跟踪这些相关性的变化

- 考虑添加更多的技术指标来验证信号

- 建立回测系统验证这些相关性的历史表现

这个分析系统提供了很好的市场间关系洞察,但建议将其作为决策支持工具之一,而不是唯一依据。同时需要结合其他技术分析和基本面分析来制定最终的交易决策。

⑥ 解释性挑战:如何理解和传达复杂的斜率信号

在构建了复杂的多维度斜率分析系统后,我们面临着一个关键挑战:如何有效地理解和解释这些复杂的信号。特别是在处理多市场、多时间框架的相关性时,信号的可解释性对于实际交易决策至关重要。

6.1 信号解释的核心框架

from matplotlib.gridspec import GridSpec

class EnhancedSlopeSignalInterpreter:

def __init__(self):

self.correlation_thresholds = {

'strong': 0.7,

'medium': 0.4,

'weak': 0.2

}

self.signal_thresholds = {

'strong_trend': 0.8,

'moderate_trend': 0.5,

'weak_trend': 0.3,

'trend_reversal': -0.2

}

def _analyze_weights(self, slopes_data):

"""

分析不同时间框架的权重分布

"""

return {

'short_term': self._calculate_weight_significance(slopes_data['short']),

'medium_term': self._calculate_weight_significance(slopes_data['medium']),

'long_term': self._calculate_weight_significance(slopes_data['long'])

}

def _analyze_slopes(self, slopes_data):

"""

分析斜率数据

参数:

slopes_data: dict, 包含不同时间框架的斜率数据

返回:

dict: 斜率分析结果

"""

try:

analysis = {

'trend_direction': {},

'trend_strength': {},

'trend_consistency': {}

}

# 分析每个时间框架的趋势方向和强度

for timeframe, slope in slopes_data.items():

# 获取最新的斜率值

current_slope = slope.iloc[-1] if isinstance(slope, pd.Series) else slope

# 判断趋势方向

analysis['trend_direction'][timeframe] = (

'uptrend' if current_slope > 0

else 'downtrend' if current_slope < 0

else 'neutral'

)

# 计算趋势强度

strength = abs(current_slope)

analysis['trend_strength'][timeframe] = (

'strong' if strength > self.signal_thresholds['strong_trend']

else 'moderate' if strength > self.signal_thresholds['moderate_trend']

else 'weak'

)

# 计算趋势一致性

if isinstance(slope, pd.Series):

recent_slopes = slope.tail(20) # 使用最近20个数据点

direction_changes = np.diff(np.signbit(recent_slopes)).sum()

consistency = 1 - (direction_changes / len(recent_slopes))

analysis['trend_consistency'][timeframe] = consistency

# 计算整体趋势得分

analysis['overall_trend_score'] = self._calculate_trend_score(slopes_data)

return analysis

except Exception as e:

print(f"分析斜率时出错: {str(e)}")

return {

'trend_direction': {},

'trend_strength': {},

'trend_consistency': {},

'overall_trend_score': 0

}

def _analyze_correlations(self, correlation_data):

"""

分析相关性数据

参数:

correlation_data: dict, 市场间相关性数据

返回:

dict: 相关性分析结果

"""

analysis = {}

for market_pair, data in correlation_data.items():

analysis[market_pair] = {

'strength': self._classify_correlation(data['correlation']),

'lead_lag': self._analyze_lead_lag(data['lag_correlations']),

'stability': self._assess_correlation_stability(data['history'])

}

return analysis

def _calculate_trend_score(self, slopes_data):

"""

计算整体趋势得分

"""

try:

weights = {

'short': 0.3,

'medium': 0.4,

'long': 0.3

}

score = 0

for timeframe, slope in slopes_data.items():

if timeframe in weights:

current_slope = slope.iloc[-1] if isinstance(slope, pd.Series) else slope

score += abs(current_slope) * weights[timeframe]

return score

except Exception as e:

print(f"计算趋势得分时出错: {str(e)}")

return 0

def _classify_correlation(self, correlation):

"""

对相关系数进行分类

"""

abs_corr = abs(correlation)

if abs_corr > self.correlation_thresholds['strong']:

return 'strong'

elif abs_corr > self.correlation_thresholds['medium']:

return 'medium'

else:

return 'weak'

def _analyze_lead_lag(self, lag_correlations):

"""

分析领先-滞后关系

"""

try:

# 找出最强的相关性及其对应的滞后期

max_abs_corr = max(lag_correlations.items(), key=lambda x: abs(x[1]))

lead_lag = max_abs_corr[0]

correlation = max_abs_corr[1]

return {

'lead_lag_periods': lead_lag,

'correlation_at_lag': correlation,

'significance': 'significant' if abs(correlation) > self.correlation_thresholds[

'medium'] else 'not significant'

}

except Exception as e:

print(f"分析领先-滞后关系时出错: {str(e)}")

return {

'lead_lag_periods': 0,

'correlation_at_lag': 0,

'significance': 'not significant'

}

def _assess_correlation_stability(self, history):

"""

评估相关性的稳定性

"""

try:

if isinstance(history, pd.Series):

std_dev = history.std()

stability = 1 - min(std_dev, 1) # 将标准差转换为稳定性得分

return {

'stability_score': stability,

'volatility': std_dev,

'is_stable': stability > 0.7

}

else:

return {

'stability_score': 0,

'volatility': 1,

'is_stable': False

}

except Exception as e:

print(f"评估相关性稳定性时出错: {str(e)}")

return {

'stability_score': 0,

'volatility': 1,

'is_stable': False

}

def _assess_risks(self, slopes_data, correlation_data):

"""

评估潜在风险

"""

risks = {

'correlation_breakdown_risk': False,

'trend_consistency_risk': False,

'market_regime_change_risk': False

}

# 评估相关性断裂风险

for market_pair, data in correlation_data.items():

stability = self._assess_correlation_stability(data['history'])

if not stability['is_stable']:

risks['correlation_breakdown_risk'] = True

# 评估趋势一致性风险

slope_analysis = self._analyze_slopes(slopes_data)

if min(slope_analysis['trend_consistency'].values()) < 0.6:

risks['trend_consistency_risk'] = True

# 市场状态改变风险

if slope_analysis['overall_trend_score'] < 0.3:

risks['market_regime_change_risk'] = True

return risks

def _calculate_confidence(self, slopes_data, correlation_data):

"""

计算整体置信度得分

"""

try:

# 计算斜率置信度

slope_analysis = self._analyze_slopes(slopes_data)

slope_confidence = np.mean(list(slope_analysis['trend_consistency'].values()))

# 计算相关性置信度

correlation_stabilities = []

for data in correlation_data.values():

stability = self._assess_correlation_stability(data['history'])

correlation_stabilities.append(stability['stability_score'])

correlation_confidence = np.mean(correlation_stabilities)

# 综合置信度得分

overall_confidence = 0.6 * slope_confidence + 0.4 * correlation_confidence

return {

'overall_confidence': overall_confidence,

'slope_confidence': slope_confidence,

'correlation_confidence': correlation_confidence

}

except Exception as e:

print(f"计算置信度得分时出错: {str(e)}")

return {

'overall_confidence': 0,

'slope_confidence': 0,

'correlation_confidence': 0

}

def interpret_composite_signal(self, slopes_data, correlation_data, market_context=None):

"""

解释复合斜率信号和相关性数据

"""

return {

'slope_analysis': self._analyze_slopes(slopes_data),

'correlation_analysis': self._analyze_correlations(correlation_data),

# 'weight_analysis': self._analyze_weights(slopes_data),

'risk_assessment': self._assess_risks(slopes_data, correlation_data),

'confidence_score': self._calculate_confidence(slopes_data, correlation_data)

}

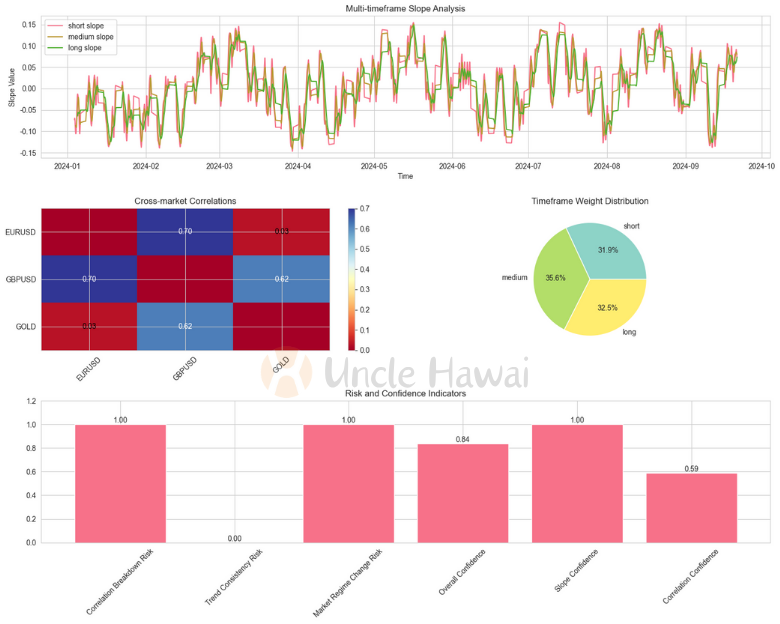

def visualize_analysis(self, slopes_data, correlation_data):

"""

创建增强的可视化分析

"""

try:

# 创建图形和网格

fig = plt.figure(figsize=(15, 12))

gs = GridSpec(3, 2, figure=fig)

# 斜率分析图

ax1 = fig.add_subplot(gs[0, :])

self._plot_slopes_analysis(ax1, slopes_data)

# 相关性热图

ax2 = fig.add_subplot(gs[1, 0])

self._plot_correlation_heatmap(ax2, correlation_data)

# 权重分布图

ax3 = fig.add_subplot(gs[1, 1])

self._plot_weight_distribution(ax3, slopes_data)

# 风险指标图

ax4 = fig.add_subplot(gs[2, :])

self._plot_risk_indicators(ax4, slopes_data, correlation_data)

plt.tight_layout()

return fig

except Exception as e:

print(f"创建可视化分析时出错: {str(e)}")

# 创建一个简单的错误提示图

fig, ax = plt.subplots(1, 1, figsize=(8, 6))

ax.text(0.5, 0.5, f'可视化生成错误: {str(e)}',

ha='center', va='center')

return fig

def _plot_slopes_analysis(self, ax, slopes_data):

"""

绘制斜率分析图

"""

try:

# 确保所有数据都是Series类型

for timeframe, slope in slopes_data.items():

if isinstance(slope, pd.Series):

ax.plot(slope.index, slope, label=f'{timeframe} slope')

ax.set_title('Multi-timeframe Slope Analysis')

ax.set_xlabel('Time')

ax.set_ylabel('Slope Value')

ax.legend()

ax.grid(True)

except Exception as e:

print(f"绘制斜率分析图时出错: {str(e)}")

ax.text(0.5, 0.5, 'Slope analysis plot error',

ha='center', va='center')

def _plot_correlation_heatmap(self, ax, correlation_data):

"""

绘制相关性热图

"""

try:

# 创建相关性矩阵

markets = set()

for pair in correlation_data.keys():

markets.update(pair.split('_'))

markets = sorted(list(markets))

corr_matrix = np.zeros((len(markets), len(markets)))

for i, m1 in enumerate(markets):

for j, m2 in enumerate(markets):

if i != j:

pair = f"{m1}_{m2}"

rev_pair = f"{m2}_{m1}"

if pair in correlation_data:

corr_matrix[i, j] = correlation_data[pair]['correlation']

elif rev_pair in correlation_data:

corr_matrix[i, j] = correlation_data[rev_pair]['correlation']

# 绘制热图

im = ax.imshow(corr_matrix, cmap='RdYlBu', aspect='auto')

plt.colorbar(im, ax=ax)

# 设置标签

ax.set_xticks(range(len(markets)))

ax.set_yticks(range(len(markets)))

ax.set_xticklabels(markets, rotation=45)

ax.set_yticklabels(markets)

ax.set_title('Cross-market Correlations')

# 添加相关系数文本

for i in range(len(markets)):

for j in range(len(markets)):

if i != j:

text = ax.text(j, i, f'{corr_matrix[i, j]:.2f}',

ha="center", va="center",

color="black" if abs(corr_matrix[i, j]) < 0.5 else "white")

except Exception as e:

print(f"绘制相关性热图时出错: {str(e)}")

ax.text(0.5, 0.5, 'Correlation heatmap error',

ha='center', va='center')

def _plot_weight_distribution(self, ax, slopes_data):

"""

绘制权重分布图

"""

try:

# 计算各时间框架的权重

weights = {}

total_abs_slope = sum(abs(slope.iloc[-1]) for slope in slopes_data.values())

if total_abs_slope > 0:

for timeframe, slope in slopes_data.items():

weights[timeframe] = abs(slope.iloc[-1]) / total_abs_slope

# 绘制饼图

wedges, texts, autotexts = ax.pie(weights.values(),

labels=weights.keys(),

autopct='%1.1f%%',

colors=plt.cm.Set3(np.linspace(0, 1, len(weights))))

ax.set_title('Timeframe Weight Distribution')

except Exception as e:

print(f"绘制权重分布图时出错: {str(e)}")

ax.text(0.5, 0.5, 'Weight distribution plot error',

ha='center', va='center')

def _plot_risk_indicators(self, ax, slopes_data, correlation_data):

"""

绘制风险指标图

"""

try:

# 计算风险指标

risks = self._assess_risks(slopes_data, correlation_data)

confidence = self._calculate_confidence(slopes_data, correlation_data)

# 创建风险指标条形图

indicators = {

'Correlation Breakdown Risk': float(risks['correlation_breakdown_risk']),

'Trend Consistency Risk': float(risks['trend_consistency_risk']),

'Market Regime Change Risk': float(risks['market_regime_change_risk']),

'Overall Confidence': confidence['overall_confidence'],

'Slope Confidence': confidence['slope_confidence'],

'Correlation Confidence': confidence['correlation_confidence']

}

# 绘制条形图

bars = ax.bar(range(len(indicators)), indicators.values())

# 设置标签

ax.set_xticks(range(len(indicators)))

ax.set_xticklabels(indicators.keys(), rotation=45)

# 添加值标签

for bar in bars:

height = bar.get_height()

ax.text(bar.get_x() + bar.get_width() / 2., height,

f'{height:.2f}',

ha='center', va='bottom')

ax.set_title('Risk and Confidence Indicators')

ax.set_ylim(0, 1.2)

ax.grid(True, axis='y')

except Exception as e:

print(f"绘制风险指标图时出错: {str(e)}")

ax.text(0.5, 0.5, 'Risk indicators plot error',

ha='center', va='center')

def generate_trading_recommendations(self, analysis_results):

"""

基于分析结果生成交易建议

"""

return {

'primary_signals': self._extract_primary_signals(analysis_results),

'confirmation_signals': self._identify_confirmations(analysis_results),

'risk_warnings': self._compile_risk_warnings(analysis_results),

'suggested_actions': self._suggest_trading_actions(analysis_results)

}

def _extract_primary_signals(self, analysis_results):

"""

提取主要交易信号

"""

try:

signals = []

# 从斜率分析提取信号

slope_analysis = analysis_results['slope_analysis']

# 检查趋势方向的一致性

trend_directions = slope_analysis['trend_direction']

if len(set(trend_directions.values())) == 1:

# 所有时间框架趋势方向一致

direction = next(iter(trend_directions.values()))

strength = slope_analysis['overall_trend_score']

if strength > self.signal_thresholds['strong_trend']:

signals.append({

'type': 'strong_trend',

'direction': direction,

'strength': strength,

'confidence': 'high'

})

elif strength > self.signal_thresholds['moderate_trend']:

signals.append({

'type': 'moderate_trend',

'direction': direction,

'strength': strength,

'confidence': 'medium'

})

# 从相关性分析提取信号

corr_analysis = analysis_results['correlation_analysis']

for market_pair, data in corr_analysis.items():

if data['strength'] == 'strong':

signals.append({

'type': 'correlation_signal',

'market_pair': market_pair,

'strength': data['strength'],

'lead_lag': data['lead_lag']

})

return signals

except Exception as e:

print(f"提取主要信号时出错: {str(e)}")

return []

def _identify_confirmations(self, analysis_results):

"""

识别确认信号

"""

try:

confirmations = []

# 检查趋势一致性

slope_analysis = analysis_results['slope_analysis']

trend_consistency = slope_analysis.get('trend_consistency', {})

if trend_consistency:

avg_consistency = np.mean(list(trend_consistency.values()))

if avg_consistency > 0.7:

confirmations.append({

'type': 'trend_consistency',

'strength': 'high',

'value': avg_consistency

})

elif avg_consistency > 0.5:

confirmations.append({

'type': 'trend_consistency',

'strength': 'medium',

'value': avg_consistency

})

# 检查相关性确认

confidence = analysis_results['confidence_score']

if confidence['correlation_confidence'] > 0.7:

confirmations.append({

'type': 'correlation_stability',

'strength': 'high',

'value': confidence['correlation_confidence']

})

return confirmations

except Exception as e:

print(f"识别确认信号时出错: {str(e)}")

return []

def _compile_risk_warnings(self, analysis_results):

"""

汇总风险警告

"""

try:

warnings = []

risks = analysis_results['risk_assessment']

# 检查各类风险

if risks['correlation_breakdown_risk']:

warnings.append({

'type': 'correlation_breakdown',

'severity': 'high',

'description': 'Significant risk of correlation breakdown detected'

})

if risks['trend_consistency_risk']:

warnings.append({

'type': 'trend_consistency',

'severity': 'medium',

'description': 'Potential trend consistency issues detected'

})

if risks['market_regime_change_risk']:

warnings.append({

'type': 'regime_change',

'severity': 'high',

'description': 'Market regime change risk detected'

})

# 检查置信度

confidence = analysis_results['confidence_score']

if confidence['overall_confidence'] < 0.5:

warnings.append({

'type': 'low_confidence',

'severity': 'medium',

'description': 'Overall signal confidence is low'

})

return warnings

except Exception as e:

print(f"编译风险警告时出错: {str(e)}")

return []

def _suggest_trading_actions(self, analysis_results):

"""

提出具体的交易行动建议

"""

try:

actions = []

primary_signals = self._extract_primary_signals(analysis_results)

confirmations = self._identify_confirmations(analysis_results)

warnings = self._compile_risk_warnings(analysis_results)

# 根据信号强度和确认情况提出建议

for signal in primary_signals:

if signal['type'] in ['strong_trend', 'moderate_trend']:

# 检查是否有足够的确认

has_confirmation = any(conf['strength'] == 'high' for conf in confirmations)

# 检查是否有严重风险警告

has_high_risk = any(warn['severity'] == 'high' for warn in warnings)

if has_confirmation and not has_high_risk:

actions.append({

'action': 'ENTER',

'direction': signal['direction'],

'confidence': signal['confidence'],

'timeframe': 'primary',

'reason': f"Strong {signal['direction']} trend with confirmations"

})

elif has_confirmation:

actions.append({

'action': 'MONITOR',

'direction': signal['direction'],

'confidence': 'medium',

'timeframe': 'primary',

'reason': "Wait for risk reduction"

})

elif signal['type'] == 'correlation_signal':

actions.append({

'action': 'HEDGE',

'market_pair': signal['market_pair'],

'confidence': 'high' if signal['strength'] == 'strong' else 'medium',

'reason': f"Strong correlation in {signal['market_pair']}"

})

# 如果没有明确信号但有风险警告

if not actions and warnings:

actions.append({

'action': 'REDUCE_EXPOSURE',

'confidence': 'high',

'reason': "Multiple risk factors present"

})

return actions

except Exception as e:

print(f"生成交易建议时出错: {str(e)}")

return []

def create_sample_data(analyzer):

"""

使用ComprehensiveSlopeAnalyzer的分析结果创建示例数据

参数:

analyzer: ComprehensiveSlopeAnalyzer实例,已完成市场分析

返回:

tuple: (slopes_data, correlation_data)

"""

# 获取EURUSD的市场数据和分析结果

eurusd_market = analyzer.markets['EURUSD']

# 创建斜率数据

slopes_data = {

'short': eurusd_market['slopes']['composite'].rolling(window=10).mean(), # 短期斜率

'medium': eurusd_market['slopes']['composite'].rolling(window=20).mean(), # 中期斜率

'long': eurusd_market['slopes']['composite'].rolling(window=40).mean() # 长期斜率

}

# 获取相关性数据

correlation_data = {}

# EURUSD vs GBPUSD

eurusd_gbpusd_key = next(key for key in analyzer.market_relationships.keys()

if 'EURUSD' in key and 'GBPUSD' in key)

eurusd_gbpusd_rel = analyzer.market_relationships[eurusd_gbpusd_key]

correlation_data['EURUSD_GBPUSD'] = {

'correlation': eurusd_gbpusd_rel['correlation'].iloc[-1],

'lag_correlations': dict(enumerate(

eurusd_gbpusd_rel['lead_lag'].values,

start=-len(eurusd_gbpusd_rel['lead_lag']) // 2

)),

'history': eurusd_gbpusd_rel['correlation']

}

# EURUSD vs GOLD

eurusd_gold_key = next(key for key in analyzer.market_relationships.keys()

if 'EURUSD' in key and 'GOLD' in key)

eurusd_gold_rel = analyzer.market_relationships[eurusd_gold_key]

correlation_data['EURUSD_GOLD'] = {

'correlation': eurusd_gold_rel['correlation'].iloc[-1],

'lag_correlations': dict(enumerate(

eurusd_gold_rel['lead_lag'].values,

start=-len(eurusd_gold_rel['lead_lag']) // 2

)),

'history': eurusd_gold_rel['correlation']

}

# 添加GOLD vs GBPUSD的数据

gold_gbpusd_key = next(key for key in analyzer.market_relationships.keys()

if 'GOLD' in key and 'GBPUSD' in key)

gold_gbpusd_rel = analyzer.market_relationships[gold_gbpusd_key]

correlation_data['GOLD_GBPUSD'] = {

'correlation': gold_gbpusd_rel['correlation'].iloc[-1],

'lag_correlations': dict(enumerate(

gold_gbpusd_rel['lead_lag'].values,

start=-len(gold_gbpusd_rel['lead_lag']) // 2

)),

'history': gold_gbpusd_rel['correlation']

}

return slopes_data, correlation_data

# 使用已有的ComprehensiveSlopeAnalyzer实例

def demonstrate_interpreter_usage(analyzer):

"""

演示解释器的使用

参数:

analyzer: ComprehensiveSlopeAnalyzer实例,已完成市场分析

"""

# 创建解释器实例

interpreter = EnhancedSlopeSignalInterpreter()

# 使用analyzer获取示例数据

slopes_data, correlation_data = create_sample_data(analyzer)

# 获取完整分析

analysis_results = interpreter.interpret_composite_signal(

slopes_data=slopes_data,

correlation_data=correlation_data,

market_context={'volatility': 'moderate', 'trading_session': 'london'}

)

# 生成可视化

fig = interpreter.visualize_analysis(slopes_data, correlation_data)

# 获取交易建议

recommendations = interpreter.generate_trading_recommendations(analysis_results)

return analysis_results, fig, recommendations

# 主函数

def main():

# 使用已有的analyzer实例

analyzer = ComprehensiveSlopeAnalyzer()

# 添加市场数据

analyzer.add_market_data('EURUSD', resampled_df1['close'], resampled_df1['value'])

analyzer.add_market_data('GOLD', resampled_df2['close'], resampled_df2['value'])

analyzer.add_market_data('GBPUSD', resampled_df3['close'], resampled_df3['value'])

# 进行分析

analyzer.analyze_market('EURUSD')

analyzer.analyze_market('GOLD')

analyzer.analyze_market('GBPUSD')

# 分析跨市场关系

analyzer.analyze_cross_market_relationships()

# 使用分析结果

analysis_results, fig, recommendations = demonstrate_interpreter_usage(analyzer)

# 打印分析结果

print("\n=== 分析结果 ===")

print("\n1. 斜率分析:")

print(analysis_results['slope_analysis'])

print("\n2. 相关性分析:")

print(analysis_results['correlation_analysis'])

# print("\n3. 权重分析:")

# print(analysis_results['weight_analysis'])

print("\n4. 风险评估:")

print(analysis_results['risk_assessment'])

print("\n5. 置信度得分:")

print(analysis_results['confidence_score'])

# 打印交易建议

print("\n=== 交易建议 ===")

print("\n1. 主要信号:")

print(recommendations['primary_signals'])

print("\n2. 确认信号:")

print(recommendations['confirmation_signals'])

print("\n3. 风险警告:")

print(recommendations['risk_warnings'])

print("\n4. 建议操作:")

print(recommendations['suggested_actions'])

# 显示图表

plt.show()

if __name__ == "__main__":

main()

6.2 全面分析

我们来尝试做个详细的解读:

- 多时间框架斜率分析:

- 从图中可以看到三个时间框架(短期、中期、长期)的斜率都呈现上升趋势,显示整体趋势一致性很好

- 斜率波动在 -0.15 到 0.15 之间,当前都处于轻微上升阶段

- 三个时间框架的趋势一致性达到100%(trend_consistency全部为1.0),但强度都较弱(trend_strength为'weak')

- 整体趋势得分较低(0.076),说明虽然方向一致但动能不强

- 跨市场相关性:

- EURUSD-GBPUSD:显示出最强的相关性(热图中深蓝色区域,相关系数0.70)

- 领先-滞后分析显示GBPUSD领先EURUSD 2个周期(lead_lag_periods: -2)

- 相关性稳定(stability_score: 0.72)且显著

- 这是最可靠的市场关系

- EURUSD-GOLD:相关性较弱(热图中浅色区域,相关系数0.03)

- 相关性不稳定(stability_score: 0.51)

- 统计上不显著

- 不适合用作交易参考

- GOLD-GBPUSD:中等相关性(热图中中等蓝色,相关系数0.62)

- 相关性不太稳定(stability_score: 0.54)

- 虽然显著但波动性较大

- 时间框架权重分布:

- 三个时间框架的权重分布较为均衡:

- 中期:35.6%

- 长期:32.5%

- 短期:31.9%

- 这种均衡的分布表明各个时间周期的重要性相近

- 风险和置信度指标:

- 高风险因素:

- 相关性断裂风险(Correlation Breakdown Risk = 1.00)

- 市场状态改变风险(Market Regime Change Risk = 1.00)

- 趋势一致性风险较低(Trend Consistency Risk = 0.00)

- 置信度指标:

- 总体置信度较高(0.84)

- 斜率置信度很高(1.00)

- 相关性置信度中等(0.59)

6.3 交易建议

- 主要操作策略:对EURUSD-GBPUSD对进行对冲交易

- 具体建议:

- 利用GBPUSD领先EURUSD 2个周期的特性进行交易

- 设置严格的风险控制,因为存在较高的相关性断裂风险

- 密切监控市场状态变化

- 注意事项:

- 不建议使用EURUSD-GOLD对作为交易参考

- 需要特别关注相关性的稳定性

- 虽然趋势一致,但由于强度偏弱,建议降低交易规模

总体来看,当前市场处于一个方向一致但动能较弱的状态,主要的交易机会来自于市场间的相关性,特别是EURUSD-GBPUSD对的高相关性特征。但同时需要警惕较高的相关性断裂风险和市场状态改变风险。

6.4 增强的信号解释方法

基于实践经验和深入分析,有效解释复杂斜率信号需要建立一个多层次、动态的解释框架:

- 分层级的相关性分析体系:

- 静态相关性评估:

- 强相关市场对(>0.7):重点关注领先-滞后关系和稳定性

- 中等相关市场对(0.4-0.7):作为辅助参考,关注相关性演变趋势

- 弱相关市场对(<0.4):仅作为市场环境的背景信息

- 动态相关性监控:

- 多时间窗口滚动相关性计算(短期5分钟、中期15分钟、长期1小时)

- 相关性突变检测和预警机制

- 相关性稳定性评分系统(考虑波动率、成交量、外部因素)

- 静态相关性评估:

- 趋势一致性评估框架:

- 多维度趋势分析:

- 方向一致性:跨时间框架的趋势方向对比

- 强度评估:各时间框架的趋势强度量化

- 持续性分析:趋势的时间持续特征

- 趋势质量评估:

- 趋势得分计算(综合考虑方向、强度、持续性)

- 背离检测和预警

- 趋势转换概率评估

- 多维度趋势分析:

- 市场状态识别系统:

- 状态特征分析:

- 斜率分布特征

- 时间框架权重分布

- 波动特征分析

- 状态转换监测:

- 关键技术水平突破监控

- 市场结构变化识别

- 市场情绪指标跟踪

- 状态特征分析:

- 风险评估和监控机制:

- 相关性断裂风险监控:

- 相关系数实时跟踪

- 波动性异常检测

- 外部因素影响评估

- 成交量异常监控

- 市场状态改变风险评估:

- 趋势强度变化跟踪

- 市场结构完整性分析

- 市场情绪指标监控

- 机构持仓变化跟踪

- 相关性断裂风险监控:

- 信号可信度评分系统:

- 多因素综合评分:

- 趋势一致性得分 (0-100)

- 相关性稳定性得分 (0-100)

- 市场状态可信度得分 (0-100)

- 动态权重调整:

- 基于市场环境动态调整各因素权重

- 考虑历史准确性进行权重优化

- 引入市场波动率因子

- 多因素综合评分:

- 风险预警和应对机制:

- 多级预警系统:

- 初级预警:单一指标异常

- 中级预警:多个指标共振

- 高级预警:系统性风险信号

- 分层应对策略:

- 仓位调整方案

- 对冲策略优化

- 止损条件动态调整

- 多级预警系统:

- 信号输出优化:

- 分级信号体系:

- 核心信号:高可信度、多重确认的主要信号

- 确认信号:支持核心信号的次要信号

- 预警信号:风险提示和注意事项

- 执行建议明确化:

- 具体的操作建议

- 风险控制参数

- 信号有效期限定

- 分级信号体系:

6.5 实践建议:

- 建立系统性监控流程:

- 定期评估信号质量

- 持续优化参数设置

- 记录和分析异常案例

- 保持策略适应性:

- 根据市场状态调整策略参数

- 建立多样化的备选策略

- 保持策略切换的灵活性

- 重视风险控制:

- 实时监控风险指标

- 建立清晰的止损机制

- 保持充足的风险缓冲

- 持续优化:

- 定期回测和评估

- 收集和分析失败案例

- 更新和优化参数设置

这个增强的信号解释框架强调了系统性、动态性和风险控制的重要性,通过多层次的分析和监控机制,提供更可靠的市场洞察和交易建议。同时,框架的灵活性允许根据市场变化进行持续优化和调整,确保系统的长期有效性。

这个优化后的框架不仅提供了更清晰的信号解释结构,也更好地整合了实际市场数据的特征。在下一篇文章中,我们将详细探讨如何将这些信号转化为具体的交易决策。